The shipping industry is the backbone of international trade and the largest enabler of globalization. According to the United Nations Conference on Trade and Development (UNCTAD), around 80% of global trade by volume and over 70% of international trade by value happens by sea. As per Drip Capital’s internal analysis, SMBs worldwide contribute over 25% of the US$ 18 trillion maritime trade. The Suez Canal blockage in March 2021 highlighted various issues faced by the shipping and logistics industry. However, Drip Capital observed that this sector has been going through a more profound and widespread crisis since the onset of the COVID-19 pandemic and the resulting economic contraction.

While every exporter and importer felt some degree of the brunt from the economic contraction, the most heavily affected were the SMB traders of the world. Mr. Jignesh Mehta from Rise and Shine Overseas, a small agri-products exporter from India, shares the panic around the shipping crisis. He said, “The entire global supply chain has been disrupted. It has become challenging to cater to the buyer’s demand because of the shortage of shipping containers. Even after getting a container, we pay astronomical ocean freight costs that we have never seen before. The agri-commodity industry operates on low-profit margins, and this spike in freight rate has been deeply cutting into our margins, and survival at times has become tough”.

Many other shippers around the world share this SMB exporter’s plight. The shortage of shipping containers has led to freight costs skyrocketing over the last year and settling on all-time highs. As of July 8th, 2021, Drewry’s composite World Container Index (WCI) -- a global index for container spot market freight rates on all the major routes, peaked at US$ 8796, up by more than 450% since the emergence of the coronavirus in December 2019.

The shipping crisis is a consequence of the uneven post-COVID-19 economic recoveries of the world’s largest importing and exporting countries. The novel coronavirus has hit the world with multiple waves and new variants. But, the difference in the degree and level of its impact on each country meant everyone around the globe experienced lockdowns and the subsequent easing of restrictions at different points in time.

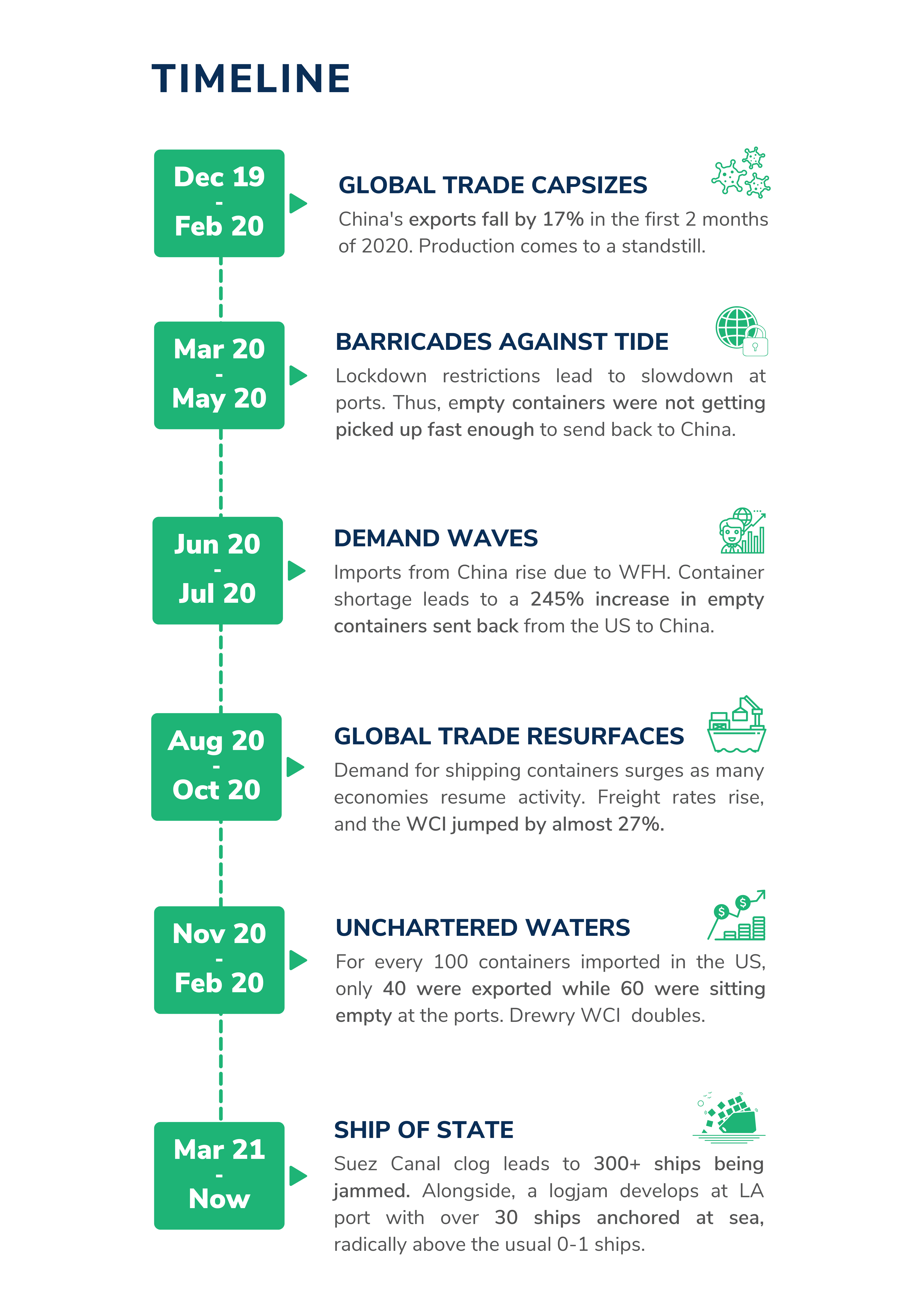

In 2019, China-- the world’s largest exporter, contributed to 16.1% of overall international exports. But when covid struck this global trade powerhouse, China’s exports plummeted by 17% in the first two months of 2020. This was due to strict lockdowns leading to a manufacturing standstill, labor shortage to transport the incoming containers, and diversion of multiple reefer containers from major Chinese ports. Consequently, shipping liners predicted a further plunge in ocean freight and began skipping docks or even the entire route to shield themselves from significant losses.

The covid-19 pandemic led to an economic contraction across the world. In March 2020, with social distancing protocols and coronavirus clusters amongst dockworkers, there emerged a shortage of containers in Asia as empty metal boxes were stranded at North American and European ports. As China started to recover from the virus and its economic impact, it was flushed with orders from North American and European markets, and it recorded a 3.5% y-o-y growth in April 2020.

Hence, China began ramping up its global empty container repositioning program. According to S&P data, in June, the total volume of empty twenty-foot equivalent unit (TEU) containers shipped from the US to China increased by 188% Y-o-Y and 245% Y-o-Y in June and July, respectively. On the other hand, more cargo came into consumer-led economies like the US, where the goods movement system had slowed down due to a lack of workforce and a series of lockdowns.

Between August and October, when the lockdown was gradually relaxed, and demand started picking up in the west, the requirements for shipping containers returned. This surge in demand, coupled with the fact that empty containers were at the wrong place at the wrong time, saw Drewry’s composite WCI jump by almost 27%, from US$ 2059 at the start of August to US$ 2615 at the end of October.

Download the Global Shipping Crisis Report