Collateral free working capital

Fund your exports growth using your foreign trade receivables.

Although factoring as a service has been around for a long time in India, it has only recently started gaining popularity as an alterntive to traditional ways of securing finance against trade payables. A factoring service is an arrangement wherein a company simply sells their trade receivables to a third party financial institution or a bank (the factor), this is also why it is popularly referred to as a Bill Purchase Solution. The first factoring solution was introduced in 1991 by SBI Global factors. Today, however, trading and manufacturing companies can choose between several bank and non-bank entities for their factoring requirements

As opposed to traditional ways of securing working capital finance, bill factoring or invoice factoring solutions have a few distinct advantages. Firstly, they're much quicker. Growing companies in India can expect disbursements directly into their account in a currency of their choice within as little as 24-48 hours. Secondly, since a factoring solution involves a direct transfer of risk to the factoring company, its far less risky for the seller who can focus on the core areas of the business instead of worrying about getting paid. Lastly, a good factoring company, with a strong global presence acts in an advisory capacity, due to their global expertise that spans several industries, factoring companies can advice companies on the best course of action

Sellers in India should seek out some basic criteria for qualifying factoring agencies. For one, the agency should have a global track record and expertise so they can navigate international markets seamlessly and work with your buyer without any hassles. Secondly, exporters can compare different factoring service providers by comparing the total funded transactions till date. Thirdly, choosing a recourse-based factoring service will undoubtedly be a lot cheaper when compared to a non-recourse service. However, the inherent risks of a recourse based factoring solution may outweigh the costs as the risks fall back upon the seller in case of a default

Over the course of more than half a decade, we've had the opportunity to perfect our offerring and affordable factoring solutions to domestic and international traders in India.

These are the typical costs of factoring with Drip Capital

Interest Rates: We charge anywhere between 0.8% Per Month to 1.4% per month to our clients, the actual interest rates vary wildly depending on the supplier's financials, the sellers track record of completing orders and the buyer's track record of successful purchases.

Processing Fees: Unlike other factoring firms, we take pride in charging some of the lowest processing fees in the industry, and on occassion, we may also waive them off

That's it, there are no other hidden costs in availing our trade factoring services.

We've compiled this article to compare general factoring costs in the market

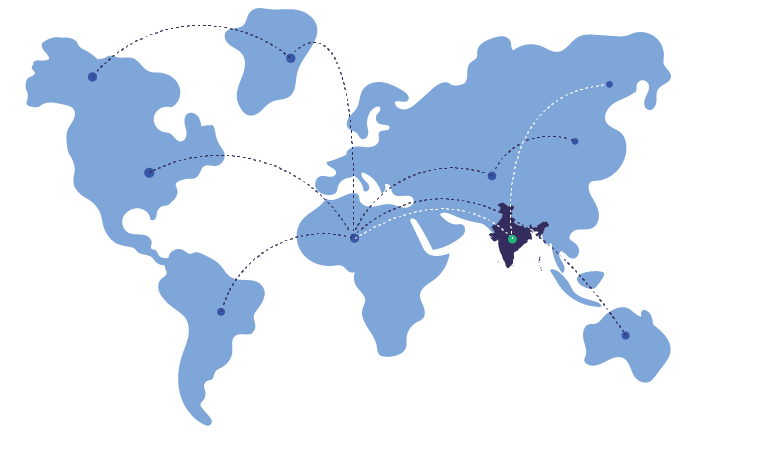

$5 Billion+

Trade Financed

6,000

Buyers & Suppliers

100+

Countries

100,000

Cross-Border Transactions

Learn about how we’ve 10xed exporters

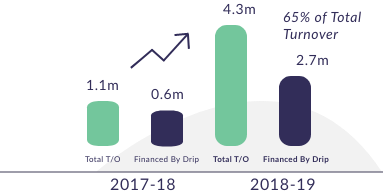

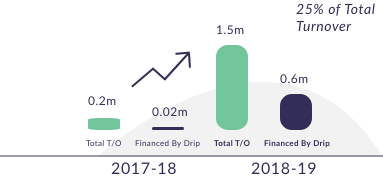

Exporter of Plastic products from Maharashtra

We started factoring our export invoices with Drip in FY17-18 and by 18-19 we were getting almost 25% of our invoices financed by them. With the boost in working capital and increased competitiveness in foreign markets because of better terms of sale, our turnover has shown a substantial increase.

Exporter of frozen foods from Andhra Pradesh

As an exporter you may have a great offering, but without easy access to short-term finance, you face challenges in scaling and have to let go of many opportunities. Drip Capital’s easy and efficient export finance solution has helped us ensure there is continuous cash flow in our business. Now we can convert possibilities which we otherwise would have passed on. The result has been a 220% jump in sales in FY19.

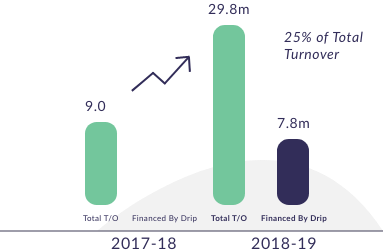

Exporter of Red chillies from Andhra Pradesh

When we started our business in 2017, traditional lending institutes could not keep up with the increasing orders from our buyers. With Drip capital fulfilling our working capital requirement, in FY 19 our business reported massive growth as compared to the previous year, over 50% of those export invoices were financed by Drip.

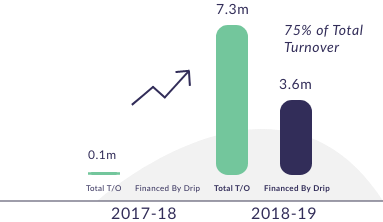

Exporter of Basmati Rice from Punjab

Drip’s factoring service has ensured that our liquidity doesn’t remain tied up in invoices for a long time. Since the start of our collaboration, we have been able to cater to more buyers and our export turnover has increased 4x between FY17-18 and FY18-19.