A letter of credit, or LC, is an assurance from the importer’s bank to the exporter that the payment for a shipment will be made by the bank to the exporter if the importer fails to make the payment.

An LC reduces the risks involved in international trade by guaranteeing the payment of funds to the exporter and timely delivery of goods for the importer.

However, while an LC assures payment, the exporter still has to wait until after the credit period to receive the sale amount. If the exporter wants the payment for the shipment to be made immediately, they can avail an LC backed bill discounting facility from their bank.

In this article, we will cover the process of letter of credit discounting, how to calculate it, and typical charges of discounting LCs in India and also a format of an LC discounting letter.

What is LC Backed Bill Discounting?

LC-backed bill discounting is a short-term credit facility provided to the seller or exporter by their bank. As the name suggests, it is used exclusively for export transactions backed by a letter of credit document when the exporter wants to receive payment for their shipment immediately, typically as an export working capital solution to fulfill the buyer’s order.

Once the exporter and importer have agreed on the transaction and the need for an LC, the importer shares an LC obtained from their bank. The exporter takes this LC and furnishes it, along with certain other documents, to their bank.

If everything is in place, the exporter’s bank will make a payment to the exporter as per the amount mentioned in the bill of exchange after deducting a discount. Through LC-backed bill discounting, the bank offers the seller immediate payment, and the buyer continues to enjoy a longer credit period.

What Are the Features of LC Backed Bill Discounting?

As the name suggests, LC bill discounting has three components – an LC, a bill, and a discounting factor.

In order to provide an LC bill discounting facility to a beneficiary, in this case the exporter, the bank requires a copy of the LC provided to the importer by their bank. Any credit provided to the exporter will be backed by this LC as the bank is assured that the exporter will receive the money from the importer and will thus be able to pay the bank back.

The bill provides the amount that the exporter is expecting as payment for the shipment.

The discounting factor is the amount the bank will deduct as its fees before making the payment to the exporter. These fees are called letter of credit discounting charges and are generally between 6 percent and 15 percent of the total bill value. The charges might vary depending on the credit period, invoice amount, and creditworthiness of the buyer. At the end of the credit period, the bank that issues the LC bill discounting collects the funds from the importer or importer’s bank if they cannot complete the payment.

Also Read : What is Factoring in Finance and How Does It Work ?

Documents Required for LC Backed Bill Discounting

Following are the typical set of documents needed to apply for LC bill discounting:

- Letter of credit from the importer

- Bill of exchange

- Commercial invoice and packing list

- Documents of title to goods evidencing the dispatch of goods or proof of delivery of goods

- Discounting request letter

- A bill of lading by the shipping line. Since LC discounting is almost always a type of post shipment finance service

Why Would a Bank Refuse to Provide LC Backed Bill Discounting Facility?

LC backed bill discounting may not be approved for all exporters as the credit risk shifts from the exporter to the bank.

A bank can refuse to issue an LC backed bill discounting for the following reasons:

- They find that the documents submitted by the exporter are not genuine.

- In cases of financial institutions that are not willing to assume transactional risks, the letter of credit or bill of exchange contains the ‘without recourse’ clause which states that the exporter cannot be held accountable if the importer does not reimburse the paying bank i.e. the LC bill discounting issuing bank.

- The bills submitted are not trade bills but are accommodation bills. Accommodation bills do not indicate a trade transaction, are not legally enforceable, and are drawn for mutual financial accommodation of the involved parties.

- The description of goods in the invoice and bill of lading does not match.

- The bill of lading has become a stale bill of lading because the exporter presented the bill of lading issued by the shipping line to their bank after the expiry date of the letter of credit.

- The shipment of goods is not properly insured

- The letter of credit is revocable i.e. the LC issuing bank can change or cancel the LC at any time without consent from any involved parties.

However, since the discounting is backed by a letter of credit, financing institutions are generally far more comfortable with discounting them as the document is backed by the importer's bank as well.

In such cases exporters can explore options apart from an LC.

How Does LC Backed Bill Discounting Work?

The LC-backed bill discounting process begins when the buyer, on the request of the seller, obtains a letter of credit from a financial institution. The letter of credit acts as a guarantee to the seller. The seller can use the letter of credit and bill of exchange to secure the funds from a financial institution.

Following is a step-by-step procedure that describes the process of the LC-backed bill discounting transaction.

- The seller and buyer enter into a sales contract for an agreed amount of goods in exchange for a certain value

- The buyer contacts the issuing bank (importer’s bank) to issue a negotiable letter of credit.

- The issuing bank creates the letter of credit and sends it to the advising bank (exporter’s bank).

- The advising bank verifies and sends the letter of credit to the seller.

- The seller ships the goods to the buyer and submits export documents to the advising bank.

- The advising bank forwards these documents to the LC issuing bank once they find them compliant.

- The LC issuing bank authenticates the export documents and communicates the acceptance of the bill under LC.

- The advising bank forwards the letter of credit to the exporter

- The letter of credit is now valid and enforced in the transaction so it can be used by the exporter to avail the bill discounting facility

- The exporter in need of funds applies for discounting of the bill backed by the letter of credit.

- The advising bank discounts the bill and advances the payment to the exporter after deducting the letter of credit discounting charges.

- On the payment due date, as described in the letter of credit, the advising bank collects the payment from the LC issuing bank.

What are the Typical LC Discounting Charges?

Like most financing solutions, the total cost of discounting an LC is divided into multiple heads, with interest rate being the biggest chunk of the total cost.

- Interest Rates: Although this varies wildly depending on the credit profile of the borrower. Data from across several leading banks in India indicate that the charges are between 7% per annum all the way uptil 12-13% per annum. A higher duration of the discounting period will result in a higher interest rate as well.

LC discounting of foreign bills are typically linked to LIBOR rates + spread.

- Processing Fee : In addition to the fixed interest rates, banks will also charge a processing fee or a bank handling fee. This will either be a flat fee or a small percentage (< 2%) of the overall facility

How are LC Backed Bill Discounting Charges Calculated?

The discounting charges are calculated according to the following formula: Discount charge = ((Funds in use x (Discount margin + Base Rate))/365) x number of days

The funds in use refers to the total invoice amount which has been submitted for discounting. Base rate is unique to every bank and the discount margin is usually quoted as a percentage over the base rate. For e.g., 2 percent over base rate.

Suppose the funds in use are INR 1,00,000 and discount margin is 3% over the base rate of 3%, outstanding for 90 days, then the discount charges will be - Discount charge = (((1,00,000 x (3% + 3%))/365) x 90 Discount charge = INR 1479.45

LC Backed Bill Discounting Limit

Banks and financial institutions that provide trade finance, working capital finance, supply chain finance, and many more funding services may fix a threshold limit for discounting the LC bill for a given period. This limit is variable and is at the discretion of the financial institution.

What is the Format of an LC Discounting Letter?

A typical request letter issued to the bank for discounting an LC, can be found here.

The following details should be mentioned in the letter before forwarding the same to the bank.

- A reference to the commercial invoice document issued at the time of sale of the goods

- A reference to the letter of credit document that is confirmed by the importer's bank

- Current account details on which the payment will be disbursed by the bank

- Any additional documents that are necessary to prove the compeletion or partial completion of the export transaction (like a bill of lading, shipping bill etc)

What are the Benefits of LC Backed Bill Discounting?

The following are the advantages of LC-backed bill discounting:

- The LC discounting facility offers the importer a longer credit period to complete payment.

- The LC bill discounting facility eliminates credit risk, as the issuing bank gives assurance to the exporter for the buyer’s obligations as stated in the letter of credit.

- On receiving the funds before the due date, the exporter can meet production-related requirements, fund newer operations, or pay off their suppliers.

- LC-backed bill discounting is a secure mode of getting funds as the bank discounts LC only after verifying the authenticity of both the parties involved in the transaction.

- This facility puts the exporter in a better position to negotiate on the basis of longer credit payment terms and helps them build a strong relationship with their trading partners.

What Happens When the Buyer Does Not Pay the Discounted Export Bills?

In the event of the importer or buyer failing to complete the payment for the goods, the bank debits the discounted amount along with interest charges from the exporter’s account. Some banks may obtain insurance against the exporters to cover default of payments in LC bill discounting.

The Export Credit Guarantee Corporation of India (ECGC) extends credit insurance coverage to banks and exporters against the risk of non-payment of goods by the buyers.

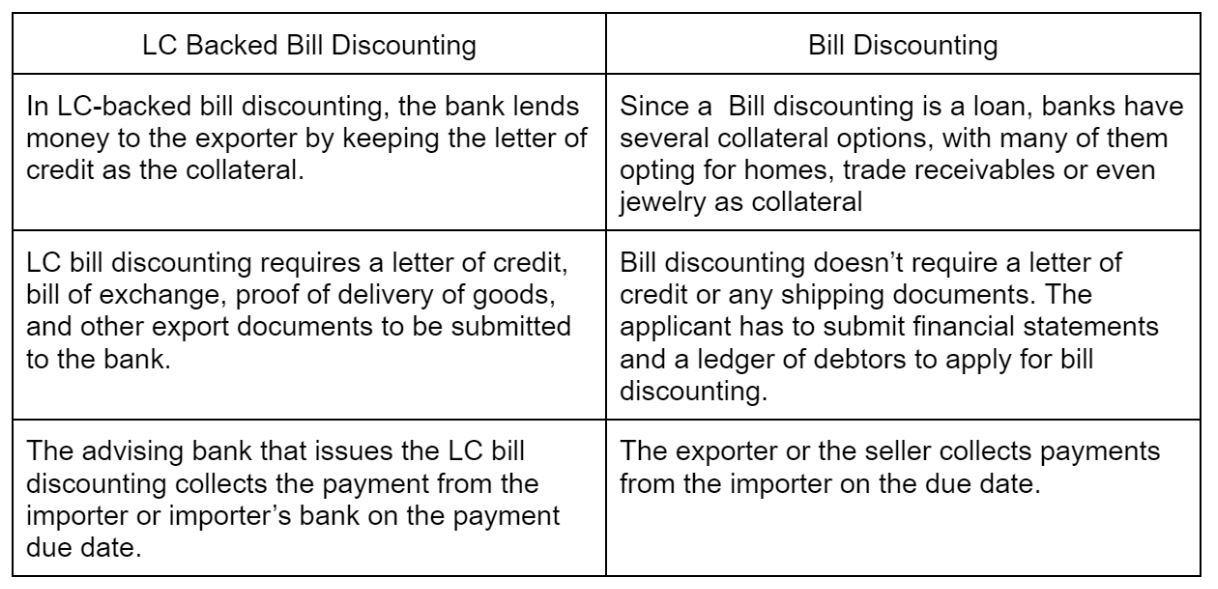

Difference Between LC Discounting and Bill Discounting

LC-backed bill discounting and bill discounting help businesses instantly access funds to meet their working capital requirements. Following are the differences between these trade finance tools:

The LC-backed bill discounting protects the interests of all parties involved in the transaction by offering advance payment to the seller and longer credit period for the buyer. It is a very useful and secure financial service that facilitates seamless international trade and helps build fruitful trading partnerships with businesses all over the world.

Can I Discount Bills without the backing of an LC?

Yes, Drip Capital's bill discounting solutions for Indian companies fund non-lc transactions that is non-recourse and can be utilized by Indian companies on-demand through our online discounting platform.