Business Line of Credit Requirements: What to Look for Before You Apply

Most business owners treat a line of credit application like a test to pass. They focus on getting approved, then sign whatever comes back. That is half the work.

In the year leading up to the Federal Reserve's most recent survey, 60% of small firms applied for financing, most often to cover operating expenses (56%) or fund an expansion (46%). A business line of credit is one of the most common tools they reach for, and for good reason: you draw what you need, when you need it, and pay interest only on what you use.

But approval is not the finish line. The terms you accept will shape your cost of capital for years. This guide splits the work in two: what lenders look for in you, and what you should look for in the line before you sign.

What a Business Line of Credit Actually Is

A business line of credit is a revolving facility. You get a credit limit, draw against it as needs come up, repay, and draw again. Interest applies only to the amount you have actually used, which sets it apart from a bank loan, where you take the full sum at once. This piece is about the decision you make before you apply.

By the numbers

What business owners are up against

60%

of small firms applied

for financing last year

42%

of applicants received

the full amount sought

59%

of borrowers signed a

personal guarantee

60%

of online-lender borrowers

paid more than expected

Source: Federal Reserve Banks, 2026 Report on Employer Firms (2025 Small Business Credit Survey)

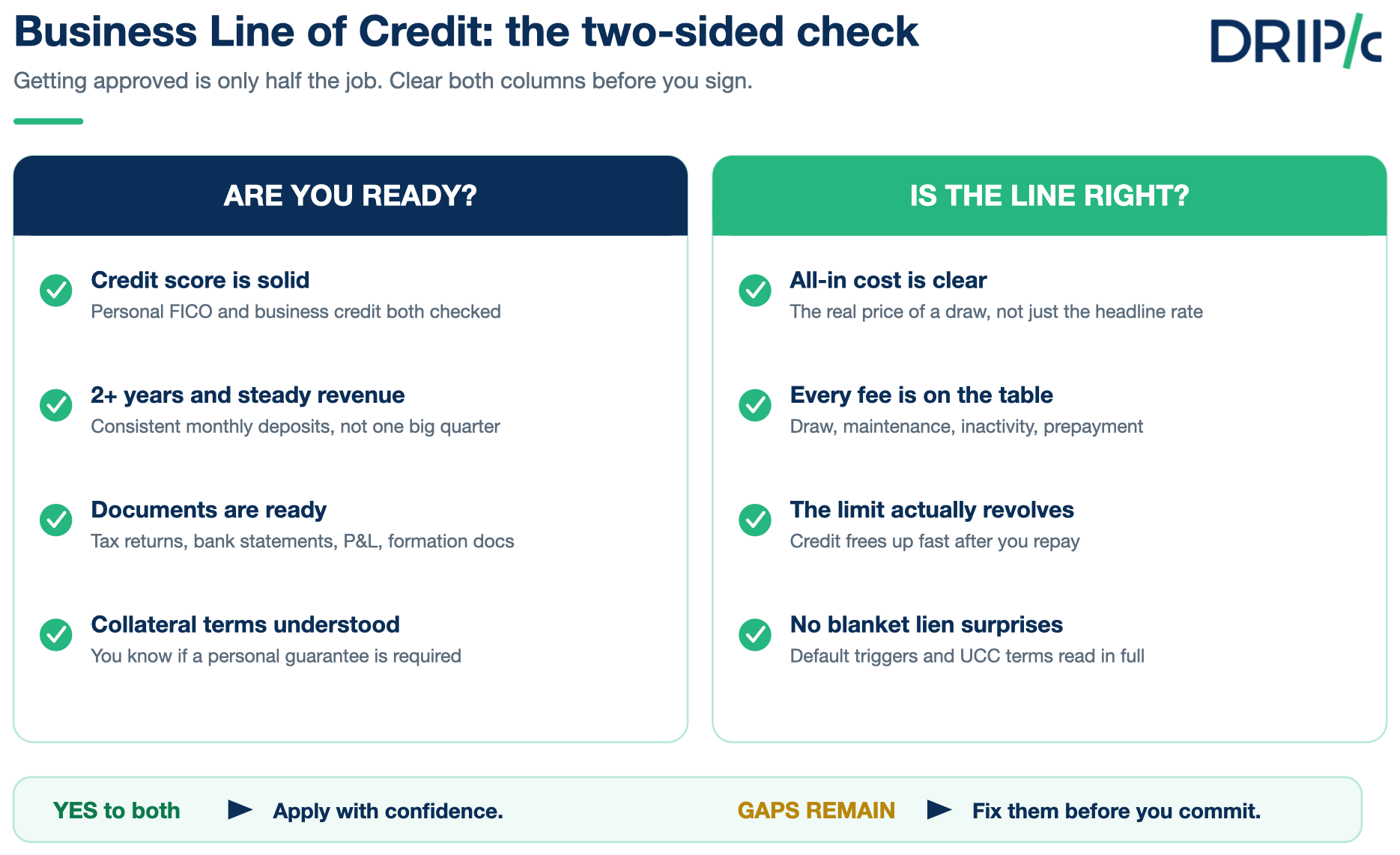

Part 1: What Lenders Look For in You

Lenders are answering one question: how likely are you to repay? Five inputs drive most of that answer. Knowing where you stand on each tells you whether to apply now or wait a quarter and fix a gap first.

Your credit score, personal and business

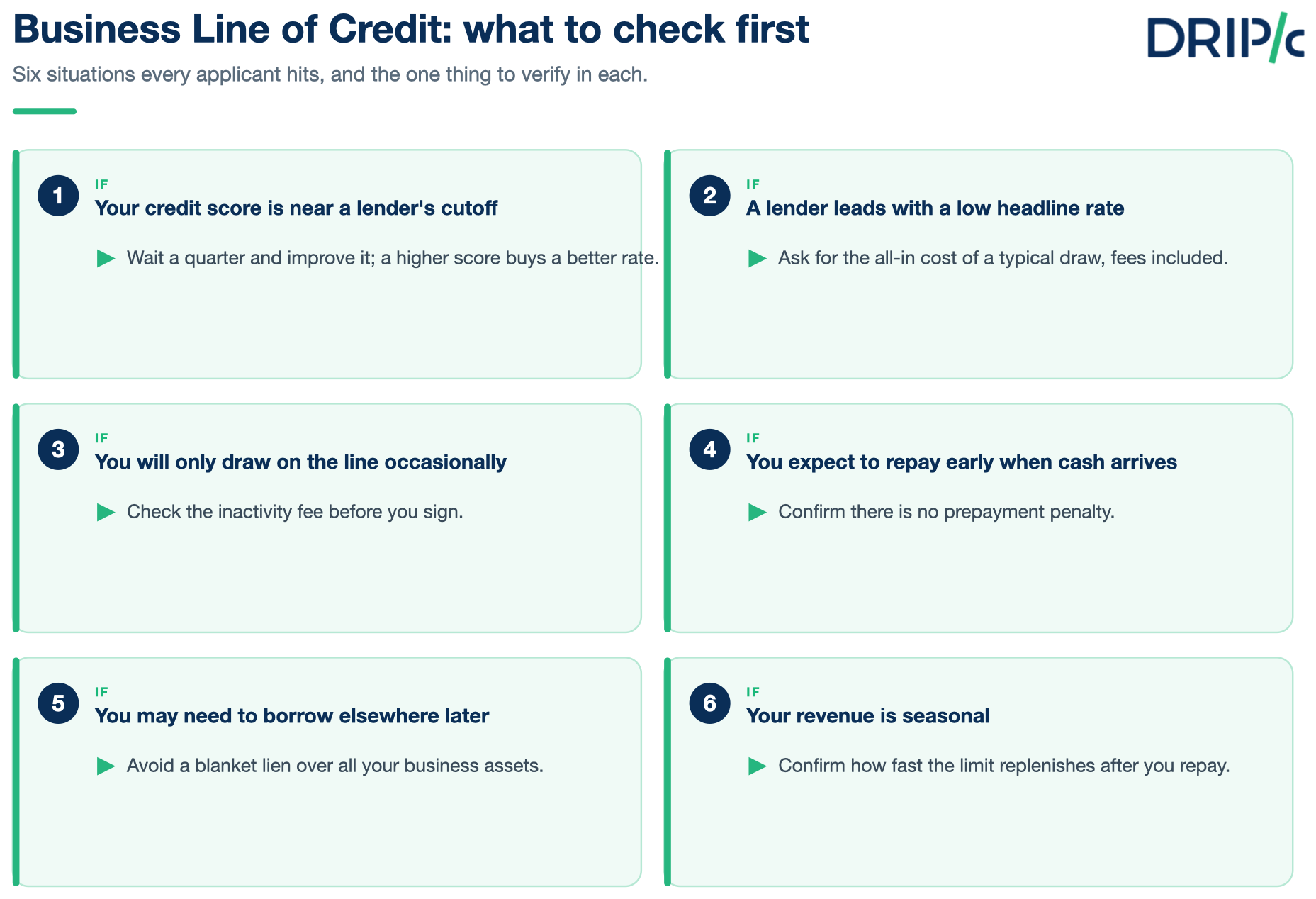

Most lenders check both your personal FICO and your business credit profile. For an unsecured line, personal credit usually carries more weight, especially for younger companies without a long business credit history. Banks tend to want stronger scores than online lenders, but a higher score almost always buys you a better rate. If your score sits near a lender's cutoff, a few months of cleanup can move you into a better pricing tier.

Time in business and revenue

Two years of operating history and steady revenue are common thresholds at banks. Newer businesses are not shut out, but they often face lower limits, higher rates, or a request for collateral. Lenders read revenue for consistency as much as size; predictable monthly deposits reassure them more than one big quarter followed by three thin ones.

The documents you will need to provide

Preparation is not a formality. Only 42% of applicants received the full amount of financing they sought; 36% got some or most, and 22% received nothing at all. A thin or disorganized application is a fast way to land in the bottom group. Have your last two years of business tax returns, recent bank statements, a profit-and-loss statement, and your formation documents ready before you start. Clean numbers tell a clearer story than a strong pitch.

Collateral and personal guarantees

Many lines are secured, and most carry a personal guarantee. Among firms that hold debt, 59% used a personal guarantee and 51% pledged business assets. A personal guarantee means your own assets are on the line if the business cannot pay. That is not automatically a bad deal, but you should know it is there before you sign.

Part 2: What to Look For in the Line Itself

Here is where most guidance goes quiet. Qualifying for a line tells you nothing about whether it is a good one. Two offers with the same headline rate can cost very different amounts once the structure is laid bare.

The real cost, beyond the rate

The advertised rate is rarely the whole price. 60% of businesses that borrowed from online lenders reported that their actual borrowing costs were higher than expected, compared with 37% at small banks and 32% at large banks. The gap is almost always in the fine print: fees, draw structures, and how interest is calculated. Ask for the all-in cost of a typical draw, the figure that reflects what you will actually pay.

Fees beyond interest

Read the fee schedule line by line. Common ones include draw fees (a percentage of each amount you pull), monthly or annual maintenance fees, inactivity fees if you do not draw, and prepayment penalties if you pay early. A line with a low rate and a stack of fees can cost more than a higher-rate line with none. Our breakdown of hidden line of credit charges shows how quickly these add up.

How the credit limit replenishes

A revolving line is only useful if it actually revolves. Confirm how fast your available credit comes back after you repay, and whether repayment is structured as flexible draws or fixed installments. Gordon, who runs a two-year-old product business in Texas, lives on this detail: his cash arrives weeks after he pays his vendors, so a line that frees up the moment he repays is worth more to him than a slightly cheaper one that does not.

Liens, UCC filings, and default triggers

Find out whether the lender files a UCC lien, and whether it is specific to the collateral or a blanket lien over all your assets. A blanket lien can block you from borrowing elsewhere. Read the default terms too: know what counts as a default, how much notice you get, and what the lender can do. These clauses rarely matter until the one quarter they matter enormously.

How to Compare Two Offers Side by Side

Once you have two offers in hand, put them on one page. List the all-in cost of a sample draw, every recurring fee, the collateral and guarantee terms, how the limit replenishes, and the default triggers. The cheaper headline rate often loses once the full picture is visible. Score the terms on their merits.

How Drip Capital's Line of Credit Handles This

Drip Capital built its Line of Credit around the terms most borrowers forget to check. There is no prepayment penalty, so paying early never costs you extra. There is no blanket lien on your assets and no UCC filing unless you default, which keeps your other borrowing options open. There is no annual maintenance fee. You draw what you need, repay over a set schedule, and your available credit comes back. The point is simple: the things you should scrutinize in any offer are the things Drip Capital chose not to charge for.

Frequently Asked Questions

What are the basic requirements for a business line of credit?

Most lenders look at your personal and business credit, time in business (often two years), and revenue consistency. Many lines are secured and carry a personal guarantee. Newer businesses can still qualify, usually at lower limits or higher rates.

What credit score do I need for a business line of credit?

There is no single cutoff. Banks generally want stronger personal scores, while online lenders accept lower ones at a higher cost. A higher score almost always earns a better rate, so it is worth checking and improving yours before you apply.

Should I choose a secured or unsecured line of credit?

A secured line usually offers a higher limit and lower rate but puts an asset at risk. An unsecured line costs more and may carry a smaller limit. Our breakdown of a secured vs unsecured line of credit walks through the trade-off in detail.

How quickly can I get a business line of credit?

It ranges from a day or two with online lenders to a few weeks with traditional banks. Having your documents ready is the single biggest factor in how fast you move from application to funding.