Unexpected cash flow issues can derail even the most profitable businesses. For example, a construction firm might secure large contracts but struggle to pay workers and suppliers due to delayed client payments. A business depends not only on how much it earns but also on how smoothly that money flows. Cash flow gaps limit growth and planning by forcing businesses to delay investments, reduce operations, or miss new opportunities.

Also Read: Impact of Automation and AI in accounts payable

In fact, a study by the U.S. Chamber of Commerce reveals that 82% of small businesses fail due to cash flow problems. Payable finance helps businesses manage cash flow by extending payment terms with suppliers. A third-party financier pays the supplier upfront, and the buyer settles the amount later. This keeps operations smooth and supplier relationships intact.

What is Payable Finance?

Payable finance (also known as supply chain finance or reverse factoring) is a set of solutions that helps businesses optimize how they handle payments to suppliers and vendors. It works by bringing in a third party, usually a financial institution or specialized platform, that pays suppliers early while allowing the buying company to pay later.

This is how it typically works:

A business buys goods or services from suppliers. For example, a U.S. retailer places a large inventory order in preparation for the holiday shopping season.

The financial provider pays the suppliers early (often with a small discount). The supplier receives the payment upfront, improving their cash flow and ensuring timely delivery.

Then the business repays the financial provider at a later date, usually on or after the original payment due date. The retailer uses revenue from holiday sales to repay the financier, easing cash flow pressure during peak season.

This arrangement benefits both the buyer and the supplier: suppliers get paid faster, improving their cash flow, while the business gains more time to pay, protecting its cash reserves.

Payable finance differs from traditional financing because it focuses on the payment process between businesses and suppliers. It ensures that both businesses and suppliers have the cash they need on time, helping maintain a smooth flow of goods and services without disrupting cash flow.

What is Cash Flow?

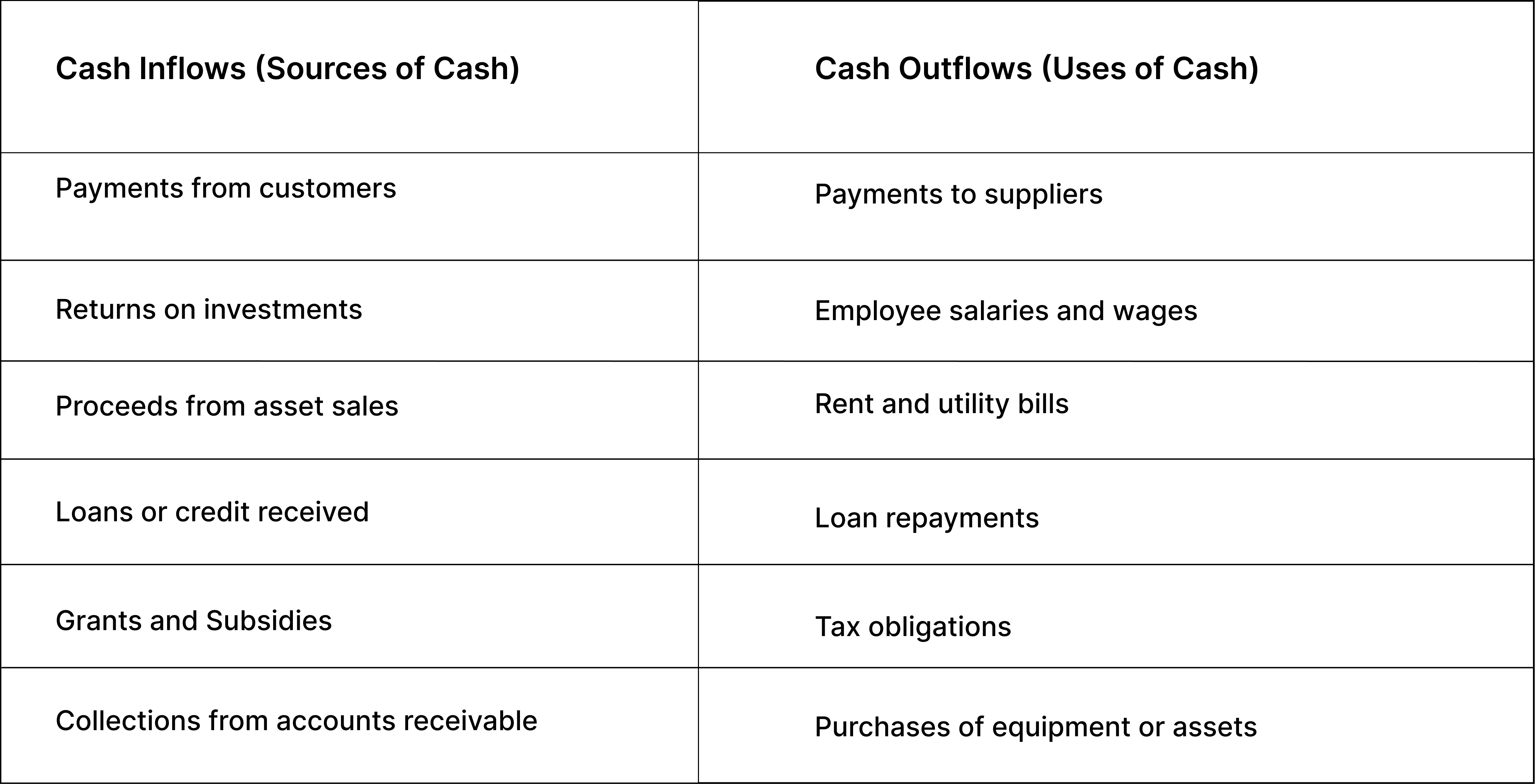

Cash flow is the movement of money into and out of a business. It represents the actual dollars coming in (inflows) and going out (outflows) of your business accounts over a specific period.

The table below illustrates common cash inflows and outflows in businesses:

When a business has more money coming in than going out during a given period, it has positive cash flow. When more money goes out than in, it has negative cash flow.

Why Does Cash Flow Management Matter?

Cash flow management is crucial for business survival and success for several reasons:

1. Day-To-Day Operations Depend on Money Management

Without adequate cash, businesses cannot pay employees, purchase inventory, or keep the lights on. No matter how profitable a company looks on paper, it needs actual cash to function day-to-day.

2. Proper Management Enables Business Growth

Having sufficient cash reserves allows businesses to invest in new opportunities such as purchasing upgraded machinery to boost production or hiring skilled staff to support growth without taking on excessive debt.

3. Financial Stability Provides Protection During Downturns

Businesses with excellent cash flow management can weather economic downturns, seasonal slumps, or unexpected challenges more effectively than those living paycheck to paycheck.

4. Affects Financing Options

Lenders and investors look closely at cash flow patterns when deciding whether to provide capital. Strong cash flow management demonstrates financial responsibility and reduces perceived risk.

5. Good Financial Management Improves Planning by Minimizing Liquidity Shocks

When business owners aren't constantly worried about making payroll or paying bills, they can make more strategic decisions focused on long-term growth rather than short-term fixes.

Benefits of Payable Finance for Cash Flow Management

Payable finance helps businesses manage money more effectively by offering greater control over outgoing payments. This supports daily operations and creates room for growth through:

Extended Payment Terms

Businesses can negotiate longer payment terms with suppliers without causing financial strain on those suppliers. This extended timeline keeps cash in the business longer, improving working capital.

Stronger Supplier Relationships

When suppliers get paid promptly through payable finance programs, relationships improve. This can lead to better terms, more reliable deliveries, and priority treatment during supply shortages.

Reduced Supply Chain Risk

By ensuring suppliers maintain healthy cash flow, businesses reduce the risk of supply disruptions caused by vendor financial problems. This creates a more stable supply chain. For example, during the Covid-19 pandemic, companies with supply chain finance programs experienced fewer disruptions. These programs provided suppliers with the necessary liquidity to continue operations despite economic challenges.

Improved Financial Metrics

Payable finance can positively impact key financial ratios like Days Payable Outstanding (DPO) and working capital efficiency, making the business more attractive to investors and lenders. For example, Coca-Cola improved its Days Payable Outstanding (DPO) through the use of supply chain finance, reducing working capital needs and making it more attractive to investors.

Cash Flow Predictability

With more control over payment timing, businesses can better predict and manage their cash position, reducing uncertainty and improving planning.

Lower Financing Costs

Payable finance generally offers lower financing costs compared to traditional loans or credit lines. This is because it relies on the buyer’s stronger credit rating, rather than the supplier's, to secure more favourable terms.

Competitive Advantage

Businesses offering early payment options to suppliers can often negotiate better pricing or priority service, creating an edge over competitors. For example, a clothing retailer that pays suppliers early can secure discounted rates on bulk orders. This allows them to offer lower prices and maintain stock availability, giving them a competitive edge over other retailers with longer payment terms.

What are the Challenges in Payable Finance?

Implementation Complexity

Setting up a payable finance program involves coordinating between multiple parties: the business, its suppliers, and financial providers. This requires significant planning and communication.

Technology Requirements

Many payable finance solutions rely on digital platforms that must integrate with existing accounting systems. This integration can be technically challenging and may require IT investments.

Supplier Adoption

Some suppliers may be hesitant to participate due to unfamiliarity with the process or concerns about changing payment terms. Providing detailed guides and direct communication about the benefits can help overcome these concerns and encourage participation.

Cost Considerations

While generally more affordable than many financing options, payable finance still comes with costs that must be carefully evaluated against the benefits. For example, a business might pay a 2% fee on a $100,000 order, totaling $2000. In contrast, a traditional loan with an 8% interest rate on the same amount would cost $8000. The savings from early payment terms must be weighed against the $6000 difference.

These challenges highlight the importance of careful planning and partnering with experienced providers when implementing supplier payment financing solutions.

How Can Drip Capital Help?

Drip Capital is a trade finance solution partner and business cash flow management platform that helps companies overcome payment delays and liquidity gaps. Drip Capital can support your business through:

Tailored Payable Finance Solutions

Drip Capital offers customized programs designed to match your specific industry requirements and business patterns. Our solutions can be adjusted based on your payment cycles, supplier relationships, and growth objectives.

User-Friendly Technology Platform

Our digital platform makes it easy to manage supplier payments, track invoices, and monitor cash flow in real-time. It is designed for quick setup, requires no complex training and integrates easily with most accounting systems, making daily operations smoother and more efficient.

Global Supplier Network

For businesses working with international suppliers, Drip Capital provides cross-border financing solutions, including working capital loans and supply chain financing. These services simplify the complexities of global trade by improving cash flow, without requiring collateral, while ensuring suppliers are paid promptly and buyers enjoy flexible terms.

Supply Chain Strengthening

Drip Capital works not only with your business but also engages directly with your suppliers to ensure smooth program adoption and maximum participation, strengthening your entire supply chain.

Flexible, Collateral-Free Financing Terms

Unlike traditional lenders, Drip Capital offers flexible terms that can adapt to seasonal fluctuations and growth phases in your business. Our solutions are also collateral-free, allowing you to access working capital without tying up assets or affecting your existing credit lines.

Managing cash flow effectively is essential for businesses to invest in growth, cover expenses on time and adjust to market changes. Payable finance offers a strategic solution to help businesses optimize payments, retain cash longer, and strengthen supplier relationships. By improving financial control and reducing supply chain risks, businesses gain a competitive edge that supports sustainable growth.

If cash flow is hindering your business growth, Drip Capital’s flexible, collateral-free payable finance solutions offer fast disbursals, helping small and mid-sized businesses maintain liquidity and stay ahead in a competitive market.

Frequently Asked Questions

1. What industries benefit most from payable finance?

Industries with long payment cycles or heavy supplier reliance benefit most. These include manufacturing, retail, construction, tech, healthcare, food and beverage, and logistics sectors, where cash flow gaps often delay operations.

2. How does payable finance differ from traditional loans?

Payable finance supports supplier payments without adding debt. It’s based on the buyer’s credit, requires no collateral, and aligns with supplier terms. Traditional loans add to liabilities, require collateral, and follow fixed repayments.

3. What’s the difference between cash flow and revenue?

Revenue is recorded when sales happen, and cash flow tracks when money actually moves. A company can earn revenue but still lack cash if payments are delayed.

4. How is payable finance different from receivable finance?

Payable finance is buyer-driven and delays outgoing payments. Receivable finance is seller-driven and speeds up incoming payments. Both improve cash flow but serve opposite ends.