Global trade transactions are tricky and rife with complexities, documentation and cultural barriers. Verifying the buyer or seller's authenticity with complete accuracy is nearly impossible.

At the same time, a free flow of finances is necessary to ensure neither of the parties are facing working capital issues. In such a situation, a seller would be wary of producing goods for the order due to the lingering uncertaintly of non-payment and the buyer or Importer would be wary of parting with him cash out of fear of the supplier's default.

Letter of credit (LC), to an extent, help with this issue and safeguard the interests of both the parties. A back to back LC aims to further safeguarf the interests of both the parties as explained below.

What is a Back to Back LC?

A back to back letter of credit involves an additional intermediary between the buyer and the seller. This intermediary is generally a bank and the entire process is divided into two LC transactions. The buyer issues an LC in favour of the intermediary and the intermediary issues an LC in favour of the buyer, while keeping the first LC as collateral.

Generally, a bank, broker or a trader acts as an intermediary between the seller and the buyer. Instead of issuing an LC to the supplier, the buyer issues it to the intermediary. This LC is called the Mast LC. The broker then submits the primary LC as collateral at a bank and asks it to issue another LC to be given to the end supplier in exchange for the shipment. The second LC that is issued keeping the primary LC as collateral is known as a 'back to back letter of credit' and the entire process is referred to as a back to back LC transaction.

If these terms are confusing, it may be a good idea to check out this article that covers the basics of what a letter of credit is and how it works in its simplest form.

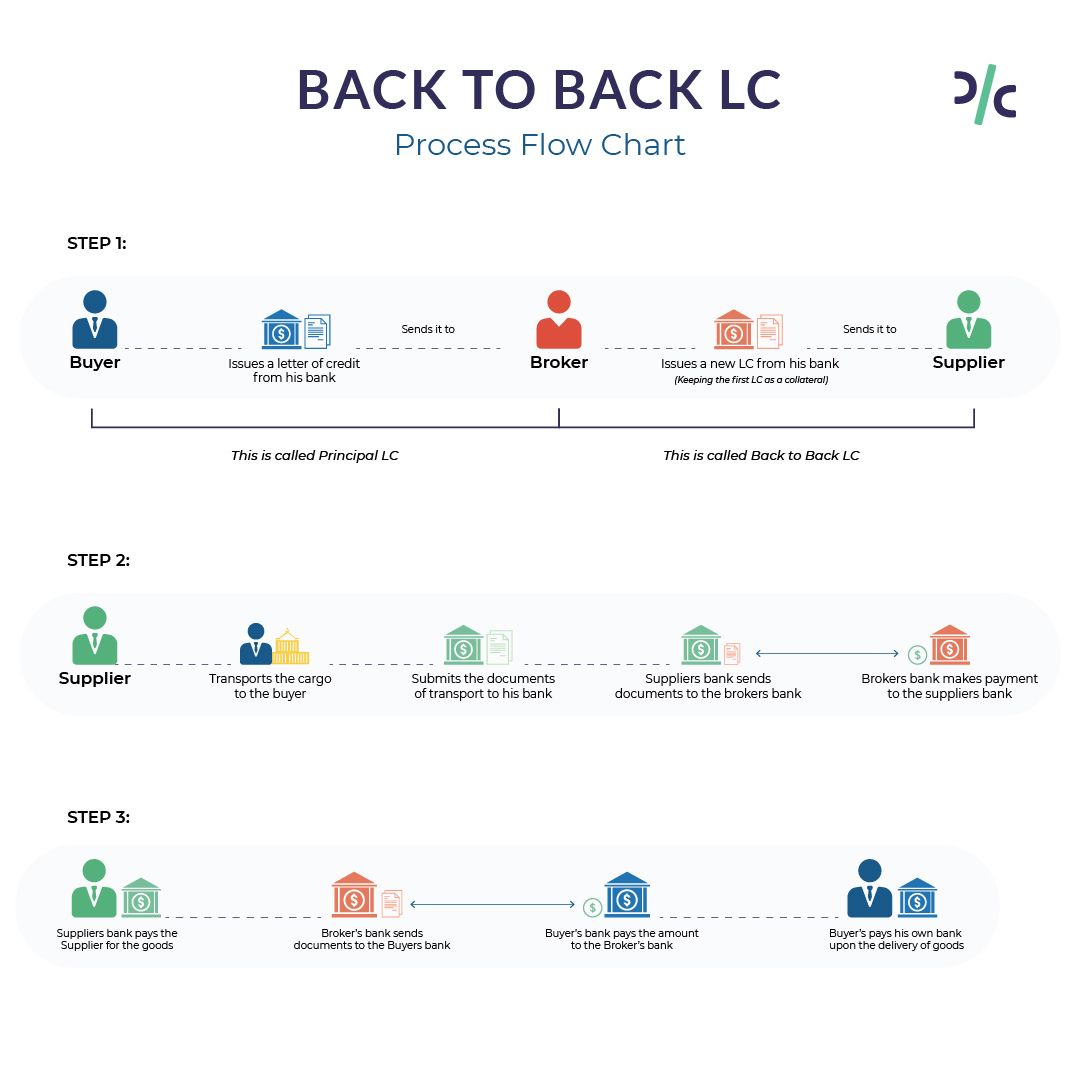

How a Back to Back LC works?

Here is a stepwise flow of how a back to back Letter of Credit works:

The first half of a back to back LC process is similar to a commercial LC. The buyer goes to his bank, also known as the issuing bank, seeking an LC to send it to the broker’s bank. This letter of credit is known as the principal LC or master LC.

The broker asks his bank to issue another letter of credit to the actual supplier, keeping the first one as collateral. This letter of credit is known as the back to back LC.

The supplier transports the cargo to the original buyer and submits the documents of transport like the bill of lading, etc. to its bank.

The supplier’s bank then sends the documents to the broker’s bank, which upon carefully scrutinizing the documents, makes the payment to the supplier’s bank.

The supplier’s bank pays the supplier for the goods.

Broker’s bank then sends the documents to the buyer’s bank. The bank scrutinizes the documents and pays the broker’s bank the amount listed in the principal LC.

The buyer pays the buyer’s bank the money upon the delivery of goods.

Terms and Conditions under Back to Back LC

- A back to back LC is issued only at the request of the beneficiary of the principal LC -- the intermediary.

- All the LCs are issued evaluating the creditworthiness of the applicant.

- There should be no disparity in the details such as product descriptions, product quantity, terms and conditions of the trade, etc. in the LCs.

- The value of a back to back LC can be a maximum of 90% of that of the principal LC. The difference is the broker’s profit margin.

- It is advisable to keep the date of shipping earlier than the date of payment of the principal LC so that the buyer receives the goods before paying for them. However, the bank is not liable for the product quality, just the documents. Hence, the LC has to be honored even in case of any defects in the products.

- The expiry date of back to back LC is always earlier than that of the principal LC.

Contents in a Back to Back Letter of Credit Format

A back to back LC looks just like a normal LC. The only difference is that it is issued by keeping the principal LC as its collateral. Here are some of the details that a back to back LC contains:

- Beneficiary Details

- Amount

- Time validity by which the payment is to be made to the bank

- Seller's Bank Details

- Payment Mode

- List of Documents

- Notifying Address

- Description of Goods

- Confirmation Order from a local Bank

Example of Back to Back LC

If company A in Germany sells automobile parts and a company C in Australia wants to buy them but are not in direct contact with one another. However, a broker B in London, who knows both the parties, enters the trade as an intermediary. He wishes to buy the parts from A and sell them to C, and earn his commission in the deal. But since both the parties do not know each other directly, there is a trust deficit between them.

Since the broker is keen on ensuring that the deal goes forward, he asks the Australian company C to apply for a letter of credit from a well known financial institution. The Australian bank, also known as the issuing bank, in this case, will look for a trusted bank in London and issue a principal LC under the broker’s name. However, the broker does not manufacture any parts. He is merely buying it from company A in Germany. So he asks his bank to keep the principal LC as collateral and issue a back to back LC to company C, which will supply the goods.

Once the supplier receives the back to back LC, they produce the shipment and send it directly to the buyer. Company A gets the money from the bank in Germany, while the buyer -- Company C pays the money to the bank in Australia.

The broker gets his profit margin, which is the difference between the amounts of both the LCs. In addition, this is how traders/buyers/suppliers/brokers eliminate credit risk with back to back LCs.

Risks under Back to Back LC

Here are some of the risks involved in dealing with a back to back letter of credit:

- If the expiry date of the master LC has been set without keeping a sufficient buffer period, it may expire before the arrival of documents from the broker’s bank. In such circumstances, the settlement becomes tricky.

- The terms and conditions of the trade may be dissimilar in the master LC and the back to back LC, or some of the other key details may be different. This leads to disparity in the documentation and often ends up making the settlement process cumbersome.

Difference between Back to Back LC and Transferable LC

A transferable letter of credit is a type of financial lending instrument where the primary beneficiary can add a secondary beneficiary who is paid the amount either partially or in full. The issuing bank has to designate such an LC as transferable at the time of issuing it. Only then can the beneficiary transfer the credit to a third party. There is only one LC involved in this process.

In the case of a back to back LC, the LC is issued by the bank against the primary LC, which acts as collateral. There are two separate LCs involved in the process- Primary LC and back to back LC.

FAQs on Back to Back LC

How do you open back to back LC?

An intermediary can ask their bank to issue a back to back LC to the supplier by submitting a principal LC as security collateral.

What is the LC front Back?

Front to Back letter of credit is a type of LC that is issued to the supplier by the broker’s bank even before they receive the principal LC.

What is a back to back guarantee?

When two different banks issue two different LCs for the same transaction -- such an arrangement is called as back to back guarantee or back to back credit. The trade generally occurs through an intermediary.

Also Read