A line of credit is widely used by businesses as a flexible financing tool for managing working capital. Instead of borrowing a fixed lump sum, businesses can access funds when needed and repay them as cash flow improves. Because of this flexibility, a line of credit is often used to manage day-to-day financial needs such as supplier payments, inventory purchases, or short-term operational expenses.

While the basic concept of a line of credit is straightforward, its real value lies in how businesses use it to maintain financial stability. When revenue cycles do not perfectly align with expenses, having access to a flexible credit facility allows companies to bridge temporary gaps without interrupting operations.

However, despite its advantages, a line of credit is not always the ideal financing solution for every situation. Businesses must evaluate both the benefits and potential drawbacks before relying on it as a primary funding source. Understanding the advantages and disadvantages of a line of credit helps businesses make better financial decisions and use this tool effectively.

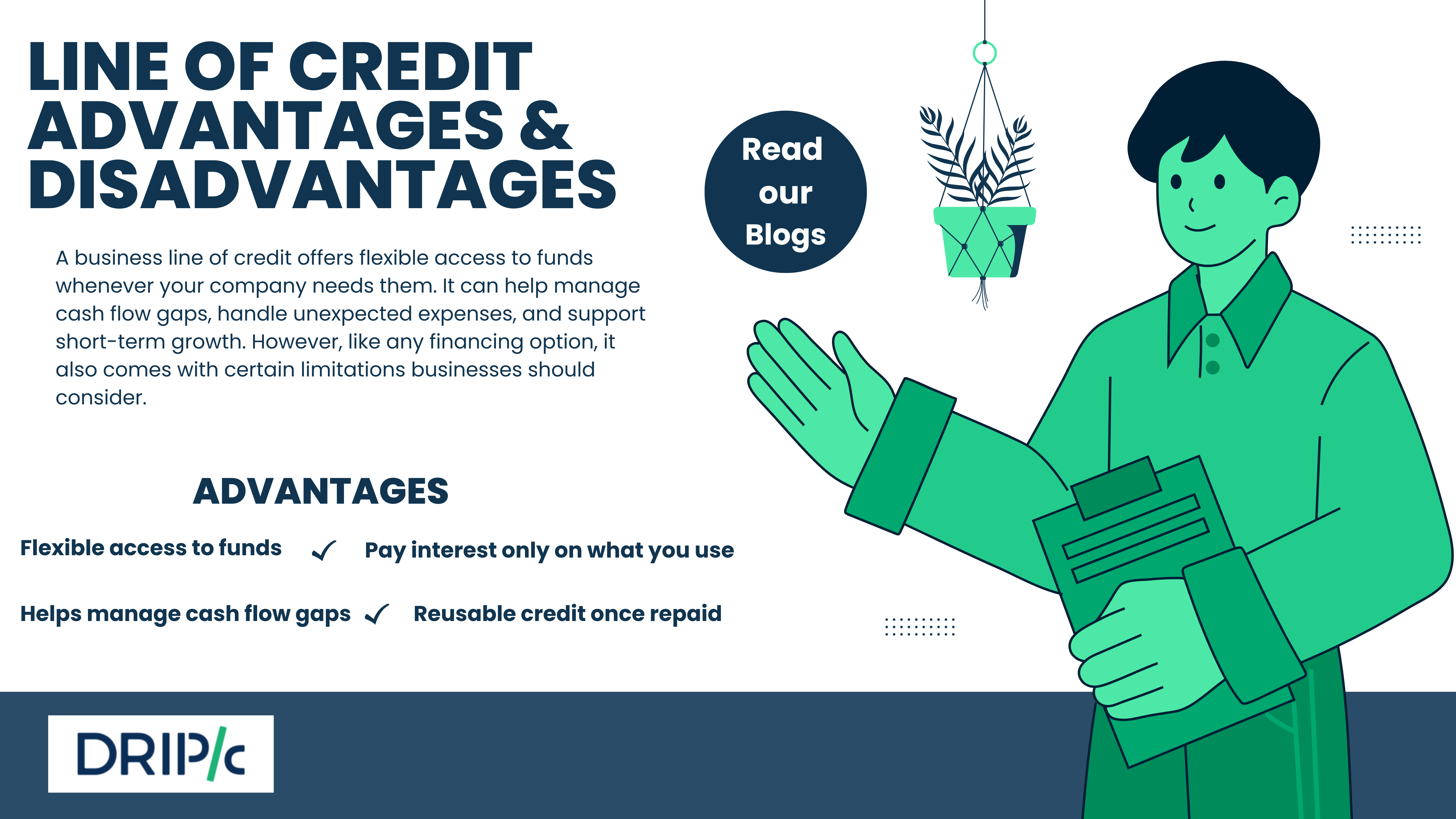

Line of Credit Advantages

A line of credit offers several benefits that make it particularly useful for businesses with recurring working capital needs. Its flexible structure allows companies to borrow only when required, making it easier to manage short-term financial fluctuations.

One of the most significant advantages is financial flexibility. Businesses rarely face predictable expenses throughout the year. Seasonal demand, supplier timelines, and operational costs can create uneven cash flow cycles. A line of credit allows businesses to respond to these situations quickly by providing access to funds whenever needed.

Another major benefit is that interest is typically charged only on the amount used, rather than the entire approved credit limit. This can make borrowing more efficient compared to traditional loans, especially when funds are required periodically rather than all at once.

Line of credit also provides continuous access to capital. Once borrowed funds are repaid, the credit limit becomes available again. This means businesses can reuse the same credit facility multiple times without submitting a new loan application.

For companies managing ongoing operational expenses, this ability to repeatedly access funds can make a line of credit an essential working capital tool.

Key advantages of a line of credit

- Borrow funds whenever required within a credit limit

- Pay interest only on the utilized amount

- Reuse the credit facility after repayment

- Quick access to funds once approved

- Useful for managing short-term cash flow gaps

Practical Use Cases of a Line of Credit

A line of credit becomes particularly valuable when businesses face timing gaps between expenses and incoming payments. Many companies must spend money upfront to keep operations running, while revenue may arrive weeks or months later. A line of credit helps bridge this gap by providing flexible access to funds that businesses can draw when needed and repay once cash inflows stabilize.

For example, a manufacturing company may need to purchase raw materials before production begins. If the business waits for customer payments before buying materials, production timelines could slow down and orders may be delayed. With a line of credit, the company can access funds immediately to keep production running smoothly and repay the borrowed amount once customers pay their invoices. However, the flexibility of a line of credit makes it useful for much more than supplier payments or invoice-related needs. Businesses often use it to manage a wide range of operational and growth expenses. A company launching a new product might draw funds to support marketing campaigns or promotional activities before revenue from the launch begins. Similarly, businesses expanding into new regions may use a credit line to cover initial setup costs such as hiring staff, onboarding distributors, or investing in logistics infrastructure.

Lines of credit are also helpful for managing ongoing operational expenses. A service-based company, for example, might use a credit line to cover payroll during periods when customer payments are delayed. Businesses may also rely on it for equipment repairs, technology upgrades, or short-term investments that improve efficiency and productivity.

Common use cases

- Purchasing inventory before peak demand periods

- Funding marketing campaigns or product launches

- Covering payroll or operational expenses during delayed payments

- Financing small equipment purchases or technology upgrades

- Supporting business expansion into new markets

- Managing unexpected short-term business expenses

Line of Credit Disadvantages

Although a line of credit offers flexibility, businesses should also be aware of certain limitations before relying on it as their primary financing option.

One concern is the risk of over-borrowing. Because funds are easily accessible, businesses may rely on credit more frequently than necessary. Without careful financial discipline, this can lead to higher debt levels and increased interest expenses over time.

Lines of credit may also come with lower borrowing limits compared to traditional loans. Businesses planning large investments such as expansion projects or equipment purchases may find that a line of credit does not provide sufficient funding.

Additionally, some lenders charge maintenance fees or administrative charges, which can increase the overall cost of the credit facility.

Key disadvantages of a line of credit

- Risk of borrowing more frequently due to easy access

- Credit limits may be smaller than traditional loans

- Possible maintenance or withdrawal fees

- Not always suitable for large long-term investments

When a Line of Credit Makes the Most Sense

A line of credit is most effective when businesses require short-term and recurring access to funds rather than a single large financing amount.

Businesses often benefit from a line of credit when:

- Cash flow cycles are inconsistent

- Operational expenses occur before revenue is received

- Funding needs arise frequently but in smaller amounts

- Working capital must be managed throughout the year

In such situations, the flexibility of a line of credit allows businesses to maintain liquidity without committing to long-term borrowing.

Frequently Asked Questions

What are the main advantages of a line of credit?

The main advantages include flexible borrowing, interest charged only on the amount used, and the ability to reuse the credit facility after repayment.

What are the disadvantages of a line of credit?

Some drawbacks include variable interest rates, potential borrowing discipline issues, and lower credit limits compared to traditional loans.

Is a line of credit suitable for working capital?

Yes. A line of credit is commonly used for working capital needs such as inventory purchases, supplier payments, and operational expenses.

Can businesses reuse a line of credit after repayment?

Yes. Once the borrowed amount is repaid, the credit limit becomes available again for future use.

Is a line of credit better than a loan?

It depends on the funding requirement. Lines of credit are generally better for short-term working capital needs, while loans are more suitable for large long-term investments.

Also Read Business Line of Credit

For immediate assistance and tailored financial guidance, speak directly with a finance specialist.Call us on +1 (650) 437-0150.