The Service Business Cash Flow Problem Is Structural, Not Situational

A service business can be profitable, growing, and well-managed - and still run out of cash. Not because something went wrong, but because of how service businesses are built.

Product companies get paid when goods ship. Service businesses get paid when clients decide to pay. That distinction sounds minor until you are looking at a $120,000 invoice on net 60 terms, payroll due in eight days, and a bank account that reflects work completed two months ago, not the work happening right now.

This is the defining cash flow challenge of service-first businesses: the work happens before the revenue arrives, and the gap between those two moments is where most financing problems live. Payroll is fixed. Overhead is fixed. Software licenses, insurance, rent - all of it runs on a schedule that does not care about your billing cycle. Revenue, on the other hand, is lumpy, delayed, and tied to payment terms that move at the client's pace.

For product businesses, lenders have a ready answer: inventory financing, purchase order financing, vendor financing. For service businesses, the answer has historically been a generic loan and the hope that the timing works out. It often does not - not because the business is weak, but because the product was never designed for this problem.

Working capital for service businesses is not a niche financing challenge. According to the SBA Office of Advocacy, small businesses contribute 43.5% of US GDP and employ 45.9% of the private sector workforce - with professional, scientific, and technical services representing one of the largest small business categories by employment. The cash flow structure that creates this problem affects the majority of American small businesses - and most of the financing products available to them were designed for a different kind of business entirely.

Why Traditional Lenders Say No to Service Businesses

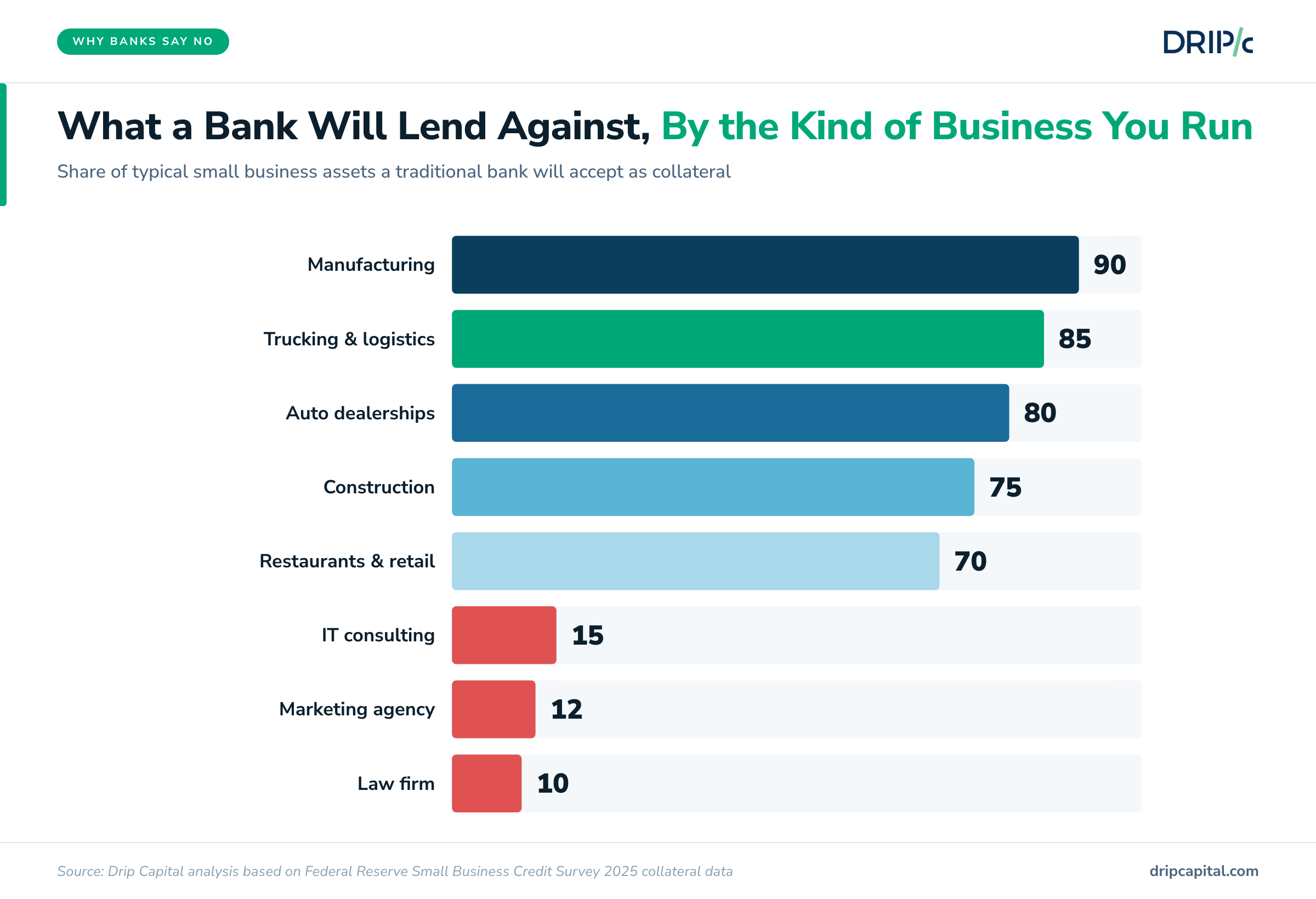

When a bank evaluates a small business loan application, it is looking for one thing above almost everything else: something it can take if the business cannot repay. Real estate, equipment, inventory, vehicles - assets with a clear market value that can be appraised, seized, and liquidated.

A service business does not have those assets. Its balance sheet is mostly receivables (money clients owe but have not yet paid), the laptops its team uses, and whatever cash is in the account. None of that satisfies a traditional collateral requirement - and without collateral, most banks simply will not lend, regardless of how healthy the revenue looks.

This is not a credit score problem or a revenue problem. It is a structural mismatch between what banks require and what service businesses can offer. The Federal Reserve's Small Business Lending Survey identifies firms whose capital is held in intellectual property rather than physical assets as being disproportionately likely to face collateral barriers - exactly the profile of a consulting firm, an IT services company, or a marketing agency.

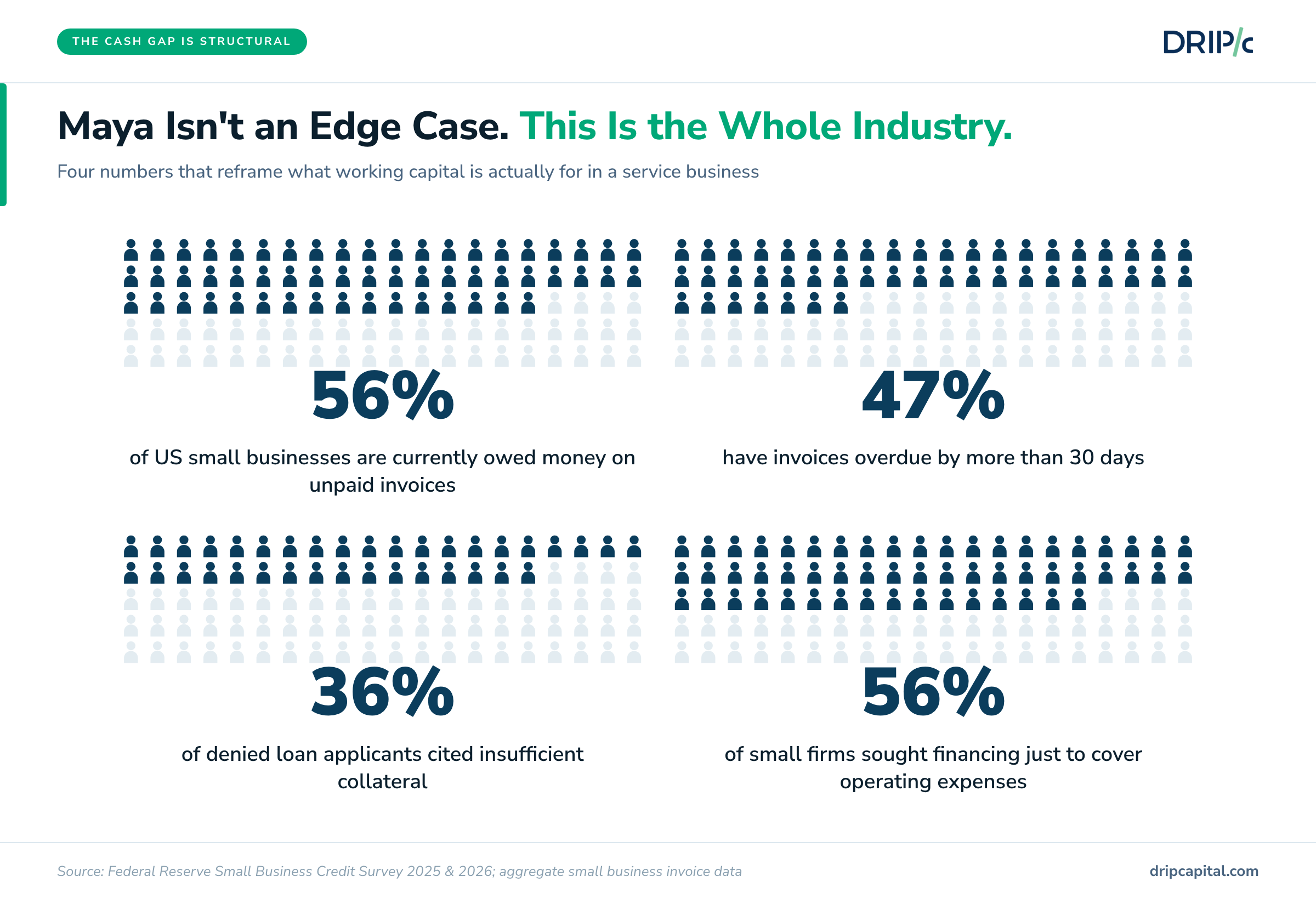

The data bears this out. According to the Federal Reserve's 2025 Small Business Credit Survey, 36% of denied or partially funded applicants cited insufficient collateral as a reason for rejection. For service-based businesses, that number skews heavily toward knowledge-based firms that have little to pledge beyond their outstanding invoices.

Banks have also been moving in the wrong direction for this segment. The Federal Reserve's Senior Loan Officer Opinion Survey found that throughout 2025, banks tightened collateral requirements for small firms across multiple consecutive quarters, while simultaneously reducing maximum credit line sizes. For a product business with equipment or inventory to pledge, tighter collateral requirements are an inconvenience. For a service business, they can be a hard stop.

The result is a financing gap that has nothing to do with whether the business deserves capital. It has to do with whether the business fits the template lenders built decades ago for a different kind of economy.

What Working Capital Challenges Look Like for a Service Business

Meet Maya. She runs a 30-person IT consulting and managed services firm. Her clients are mid-market and enterprise companies across healthcare and financial services - her work ranges from infrastructure projects to ongoing support retainers. Five years in, her pipeline is strong, her team is capable, and her client relationships are solid.

Her biggest financial challenge has nothing to do with any of that.

A healthcare client - one of her largest - is on net 60 terms. A financial services firm she onboarded six months ago pays on net 45. A government-adjacent project she completed last quarter is still pending sign-off on the final invoice - which, once approved, will trigger a further 30-day payment window. Maya is not waiting on bad debt. She is waiting on good clients who pay slowly, as large organizations routinely do.

Here is what a typical month looks like for Maya in dollar terms.

Her monthly operating costs run at approximately $185,000: payroll for 30 people ($140,000), software licenses and tools ($18,000), office and infrastructure costs ($15,000), and miscellaneous overhead ($12,000). Her monthly revenue, on paper, is $220,000. The business is profitable.

But of that $220,000, approximately $90,000 is sitting in outstanding invoices that have not yet cleared. The cash that actually lands in her account this month reflects work she delivered 45 to 60 days ago - not what she is delivering right now. The gap between what she is owed and what she can spend is real, recurring, and growing as her business scales.

Maya has tried to solve this the conventional way. Her bank offered her a line of credit conditional on pledging business assets she does not have, at a limit that would not cover two weeks of payroll. A term loan application went nowhere because her balance sheet showed more receivables than hard assets. She is profitable, creditworthy, and completely underserved by the financing products available to her.

Her primary asset is $90,000 in outstanding receivables from companies like the ones her bank approves loans for every day.

What the Data Says About Cash Flow in Service-First Businesses

Maya's situation is not an edge case. It is the operating reality for the majority of service businesses in the United States.

56% of small businesses are currently owed money from unpaid invoices, averaging $17,500 per business - and that figure reflects the broader small business population. For service businesses, where every dollar of revenue arrives as an invoice rather than a point-of-sale transaction, the exposure is structurally higher. There is no inventory to sell, no product to ship: the invoice is the only mechanism through which revenue enters the business.

47% of businesses reported that a portion of their invoices were overdue by more than 30 days - meaning that for nearly half of all small businesses, the payment timeline clients agreed to is not the payment timeline clients are keeping. For a service-based business operating on net 30 or net 60 terms, a client paying 30 days late is not a minor inconvenience - it is a second billing cycle of waiting on revenue that was already delayed.

The financing data compounds the picture. 56% of small firms sought financing specifically to meet operating expenses (Federal Reserve SBCS 2026) - not to fund growth or acquire assets, but simply to cover the costs of running the business while waiting on revenue to arrive. For service businesses with no inventory and no physical assets to leverage, that financing need is almost entirely driven by the receivables gap.

The throughline across all of this data is consistent: working capital for service businesses is not a solvency problem. It is a timing problem. The revenue exists. The clients are creditworthy. The business is viable. The gap is simply the distance between when work is delivered and when payment arrives - and that gap has a financing solution that most service business owners have never been pointed toward.

Why Traditional Working Capital Financing Falls Short

The problem is not that Maya cannot find financing. It is that the financing available to her was designed for a different kind of business. Here is what that looks like in practice.

When a Term Loan Creates Fixed Debt Against Variable Revenue

A term loan gives Maya a lump sum upfront, with fixed monthly repayments on a set schedule. The structure works well when revenue is predictable and the capital need is a one-time event - buying equipment, funding a renovation, acquiring a business. It does not work well when the cash flow problem is recurring and the revenue is lumpy.

Maya's situation is not a one-time gap. It is a permanent feature of her business model: she delivers work, invoices clients, and waits. That cycle repeats every month. A term loan addresses the symptom once (the cash shortfall in a specific month) but does not address the structure that creates it. She repays on a fixed schedule regardless of whether her largest client paid on time this month - and if they did not, she is now managing both the original cash gap and a loan repayment on top of it.

For service businesses with irregular revenue cycles, fixed debt obligations are a poor structural match. The repayment does not flex when the revenue does not arrive.

When a Bank Line of Credit Requires Assets You Don't Have

A working capital loan from a traditional bank sounds like the right product for Maya's problem: draw when needed, repay when revenue arrives, repeat. In theory, it is. In practice, the bank's underwriting requirements get in the way.

Traditional bank lines of credit for small businesses typically require a combination of: business assets as collateral, a minimum credit score (often 680 or above), two or more years of tax returns, and demonstrated revenue consistency. Maya has the revenue and the credit history. What she does not have is collateral - because her business, like most service businesses, runs on people and receivables rather than equipment and inventory.

The bank looks at her balance sheet, sees $90,000 in outstanding receivables and relatively few hard assets, and either declines the application or offers a credit limit so small it does not cover the actual gap. The irony is that the receivables her bank cannot lend against are owed by the same kinds of companies her bank approves loans for.

When a Merchant Cash Advance Costs More Than the Problem It Solves

A merchant cash advance (MCA) is often the product that finds service businesses when nothing else has worked. It is fast, accessible, and requires minimal documentation. It is also one of the most expensive forms of short-term financing available - with effective annual percentage rates that routinely run between 40% and 150% depending on the provider and the repayment term.

MCAs work by advancing a lump sum in exchange for a fixed percentage of future revenue, collected daily or weekly. For a business with high daily card transaction volume (a restaurant, a retailer), that structure makes some sense. For a service business like Maya's, where revenue arrives in large, irregular invoice payments rather than daily card transactions, the daily collection model creates a new cash flow problem on top of the original one.

The MCA solves the immediate gap. It does so at a cost that frequently exceeds the value of the capital itself - particularly when the underlying problem is a timing issue that a better-structured product could address at a fraction of the price.

What Actually Works for Service Businesses

The financing products that work best for service businesses share one characteristic: they are built around the asset a service business actually has (outstanding invoices from creditworthy clients) rather than the assets it does not have (equipment, inventory, real estate).

Accounts Receivable Financing - Unlocking Capital You've Already Earned

Accounts receivable financing (also called invoice financing or receivable financing) is the most structurally precise solution for Maya's problem. Rather than taking on new debt and repaying it from general cash flow, she advances against invoices she has already issued - invoices that represent work she has already delivered, to clients who have already agreed to pay.

Here is how it works in practice. Maya completes a project for her healthcare client and issues a $60,000 invoice on net 60 terms. Rather than waiting 60 days for payment, she works with a receivable financing provider, who advances her a percentage of that invoice value (typically 80 to 90%) immediately. When the client pays at the end of the 60-day term, the remaining balance is released to Maya minus the financing fee. The facility closes with that transaction.

The underwriting logic is fundamentally different from a bank loan. The financing provider is not primarily evaluating Maya's balance sheet or her hard assets. It is evaluating the creditworthiness of her client - the healthcare company that will ultimately pay the invoice. Maya's primary asset - her outstanding invoices from large, creditworthy organizations - is exactly the collateral this product is built around.

For service businesses that work with mid-market and enterprise clients, this is a meaningful structural advantage. The larger and more creditworthy the client base, the more accessible and cost-effective accounts receivable financing becomes. Maya's bank cannot lend against her receivables - a receivable financing provider sees those same receivables as the strongest possible collateral.

Accounts receivable financing is also self-liquidating in a way that a term loan is not. The facility is tied to a specific invoice and repaid when that invoice is paid. There is no fixed monthly repayment regardless of revenue - the financing cycle closes when the transaction closes.

A Flexible Line of Credit as an Operational Buffer

Accounts receivable financing solves the invoice-specific cash gap cleanly. It does not solve the operational layer: the fixed costs (payroll, software, rent, insurance) that run every month regardless of which invoices have cleared and which have not.

A flexible line of credit addresses this layer. Rather than drawing against a specific invoice, Maya draws against a revolving credit limit when operational costs arrive before revenue does. She repays as invoice payments clear - and the credit becomes available again for the next draw.

The key distinction from a traditional bank line is the underwriting approach. A working capital facility from a digital or alternative lender evaluates Maya's revenue history, cash flow patterns, and overall business health rather than demanding hard collateral she does not have. The facility is designed for the cash flow profile of a service business - lumpy revenue, fixed costs, recurring timing gaps - rather than for a balance sheet heavy with physical assets.

For Maya, a flexible line of credit sitting alongside her receivable financing facility means she is never choosing between making payroll and waiting for an invoice to clear. The two products cover different parts of the same underlying problem - one is transaction-specific, the other is operational.

Using Both Together

The most effective working capital strategy for a growing service business is not one product or the other. It is both, deployed for the jobs each one is actually built for.

Accounts receivable financing handles the invoice-specific gap: a large project invoice sitting at net 60, a delayed government payment, a client who consistently pays late despite agreed terms. Each draw is tied to a specific receivable and repaid when that receivable clears.

A flexible line of credit handles the operational layer: payroll week when three invoices are outstanding simultaneously, a software renewal that lands in a slow month, an insurance premium that arrives before Q1 revenue has fully cleared.

Used together, they cover the full cash flow structure of a service business - the transaction gaps and the operational gaps - without forcing the business to take on generalized long-term debt to solve what is fundamentally a timing problem.

How Drip Capital Supports Service-First Businesses

Drip Capital's financing products are built for businesses that have strong client relationships and outstanding invoices - businesses where the revenue is real, the clients are creditworthy, and the only problem is timing.

For service businesses like Maya's, two products are particularly relevant.

Drip Capital's Receivable Financing advances capital against invoices Maya has already issued. She delivers the work, issues the invoice, and rather than waiting 45 or 60 days for payment to arrive, she accesses the majority of that invoice value immediately. When her client pays, the facility closes. The underwriting is anchored to her client's creditworthiness - not her hard assets - which means the same enterprise relationships that make her business valuable are what makes her financeable.

Drip Capital's Flex Line of Credit sits alongside the receivable facility as an operational buffer. Maya draws when fixed costs arrive before invoice revenue does, repays as payments clear, and the credit replenishes for the next draw. Repayment is structured across six installments, giving her a predictable schedule rather than a lump-sum due date. There is no prepayment penalty - if a payment clears early and she wants to repay ahead of schedule, there is no cost to doing so.

A few things worth knowing upfront on the Flex LOC: there is a draw fee of 3% on each draw, a wire fee of $15 per draw, and an inactivity fee applies if no draw is made in a given quarter. No blanket lien is placed on business assets unless there is a default.

The application process for both products is digital and designed to move faster than a traditional bank. For a business like Maya's - where a delayed invoice can create a payroll gap within days - the speed of access matters as much as the structure of the product.

If your business delivers services to creditworthy clients, invoices on net 30 to net 90 terms, and regularly runs into the gap between when work is delivered and when payment arrives, Drip Capital's products are worth exploring. You can learn more and apply at dripcapital.com.

Frequently Asked Questions

What is working capital for a service business?

Working capital for service businesses refers to the funds needed to cover day-to-day operating costs (payroll, software, rent, insurance) while waiting for client invoices to clear. Unlike product businesses, which can use inventory or equipment as collateral, service businesses carry most of their value in outstanding receivables - making traditional working capital products a poor structural fit and purpose-built solutions like accounts receivable financing a more natural match.

Why do service businesses struggle to get traditional bank loans?

Traditional bank loans are underwritten against hard assets: real estate, equipment, inventory. Service businesses have few of these assets - their balance sheets are mostly receivables and human capital. Without collateral to pledge, banks either decline applications outright or offer credit limits too small to address the actual gap. This is a structural mismatch, not a reflection of business quality.

What is accounts receivable financing and how does it work?

Accounts receivable financing (also called invoice financing) advances capital against invoices a business has already issued. A financing provider advances a percentage of the invoice value (typically 80 to 90%) immediately after the invoice is issued - and the remainder is released when the client pays, minus the financing fee. The facility is self-liquidating: it closes when the invoice is paid, with no fixed monthly repayments tied to general cash flow.

Is accounts receivable financing the same as invoice factoring?

They are similar but not identical. In both cases, outstanding invoices are used to access capital before the client pays. The key difference is in the collection process: with invoice factoring, the financing provider typically takes over collection of the invoice directly from the client. With accounts receivable financing, the business retains the client relationship and collection responsibility. For service businesses with long-term enterprise client relationships, the latter is usually the preferable structure.

Can a service business use a line of credit alongside receivable financing?

Yes - and for most growing service businesses, using both together is the most effective approach. Accounts receivable financing handles transaction-specific gaps (a large invoice on net 60, a delayed government payment). A flexible line of credit handles the operational layer (payroll, overhead, fixed costs that run regardless of which invoices have cleared). The two products complement each other without overlap.

What size service business is a good fit for accounts receivable financing?

Accounts receivable financing works best for businesses that invoice creditworthy clients on net 30 to net 90 terms - typically mid-market and enterprise buyers rather than individual consumers. The minimum invoice size and business revenue requirements vary by provider. Drip Capital works with businesses across a range of sizes - the most important qualifying factor is the creditworthiness of the clients being invoiced, not the size of the business itself.

How quickly can a service business access funds through receivable financing?

With a digital lender like Drip Capital, the process moves significantly faster than a traditional bank. Once a facility is established and an invoice is submitted, funds can typically be accessed within 24 to 48 hours. For service businesses where a single delayed payment can create an immediate operational gap, that speed is as important as the structure of the product itself.

What is the difference between a working capital loan and accounts receivable financing?

A working capital loan provides a lump sum or revolving credit repaid from general business cash flow on a fixed schedule. Accounts receivable financing is tied to a specific invoice and repaid when that invoice is paid - it does not add fixed debt obligations to the business's balance sheet. For a service business whose cash flow problem is timing rather than solvency, accounts receivable financing is typically the more precise and cost-effective solution.