Most businesses don't have a revenue problem. They have a timing problem.

You shipped the goods. You sent the invoice. The work is done. But your customer is sitting on a 60 or 90-day payment cycle, and your freight partner, your raw material supplier, and your monthly overhead don't care about that. They want to get paid now.

That gap between what you're owed and what you owe right now, is the exact problem invoice financing was built to solve.

It's not a new concept. Businesses have been using invoice financing against receivables for decades. But it's still one of the most misunderstood working capital tools out there, particularly for smaller businesses who assume it's only for large corporations. It's not.

This guide breaks down everything, from how invoice financing works and what it costs, to how it compares to loans, factoring, and purchase order financing.

What Is Invoice Financing?

Invoice financing is when a business uses its outstanding invoices to access cash before those invoices are actually paid.

You've done the work and issued an invoice, say for $100,000, due in 60 days. Rather than waiting two months to see that money, you take that invoice to a finance provider. They advance you a portion of it, typically 70% to 80% of the face value, right away. When your customer pays, the provider releases the remaining balance minus their fee.

That's it. No inventory to pledge, no property to put up. The invoice itself is the asset.

Invoice financing goes by a few different names depending on who you're talking to. Accounts receivable financing, invoice discounting, debtor financing. In trade contexts, it often comes up under supply chain finance or supplier financing. The names shift but the underlying mechanic is the same: you're converting a receivable into immediate cash.

How Does Invoice Financing Work?

The process isn't complicated, and for most businesses it becomes routine once they've done it a few times. Here's how it typically flows:

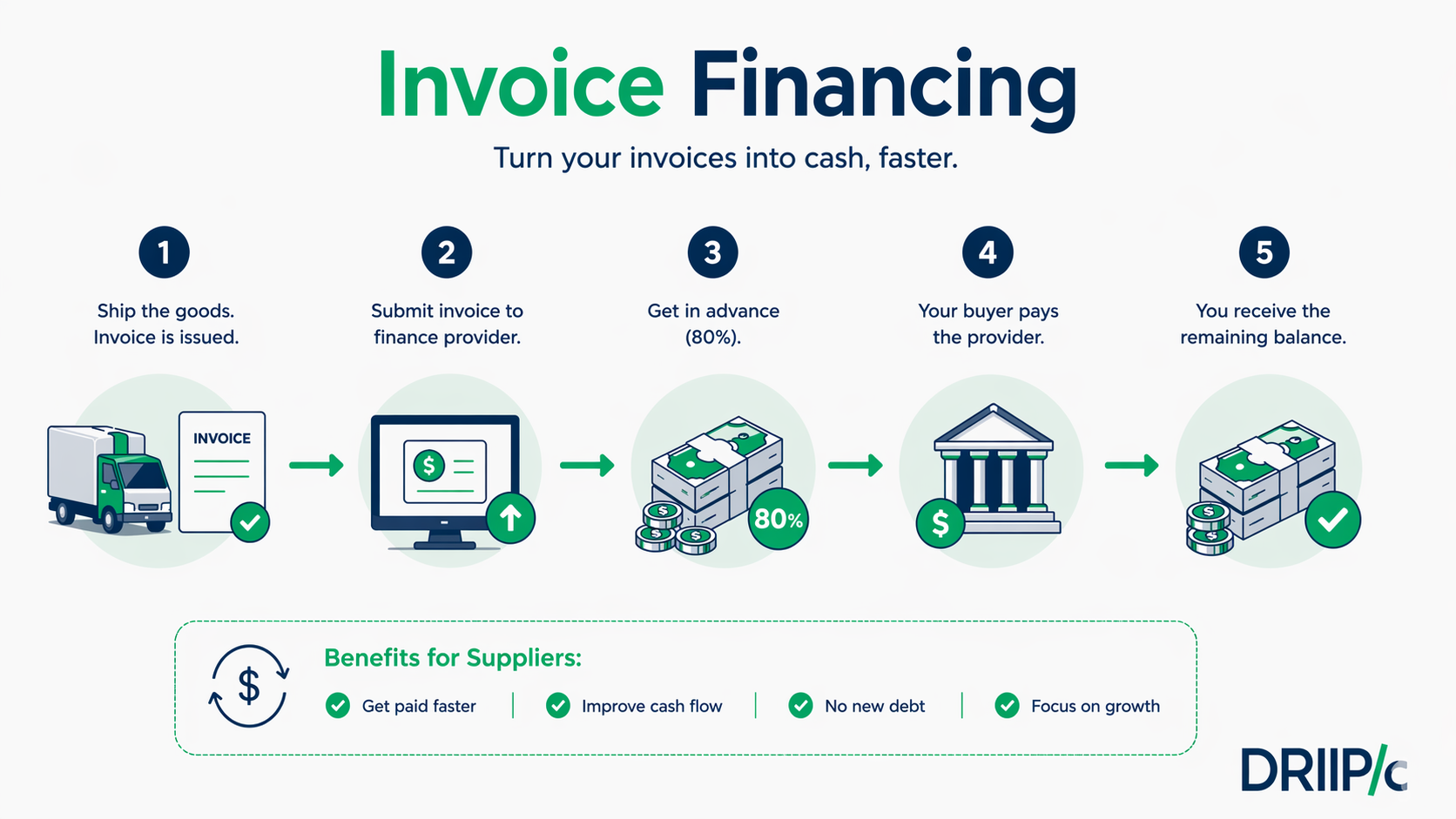

Step 1 Ship the goods . The invoice goes out. Payment terms are agreed, usually 30 to 90 days.

Step 2 Submit the invoice to your finance provider. They'll review the invoice and look at your buyer's creditworthiness.

Step 3 Get the advance. The provider pays you 70% to 80% of the invoice value. How much depends on the invoice size, your industry, and how reliable your buyer is.

Step 4 Your buyer pays. Payment goes to the provider, either directly or through your own accounts, depending on what's been agreed.

Step 5 You receive the remainder. After the provider takes their fee, the leftover balance comes to you.

Because invoice financing is always tied to a specific, real invoice, there's no borrowing against projected revenue or theoretical future sales. You're drawing on money that's already owed to you.

Invoice Financing in Practice

Let's put actual numbers to it.

A wholesale distributor has $500,000 in outstanding invoices, all sitting on 60-day terms. They need to pay a freight partner and restock before month-end. That's two weeks away. Waiting on customer payments on the buyer's side isn't an option.

They submit $300,000 in invoices through an invoice financing arrangement.

The provider advances 80% = $240,000 within 48 hours. The distributor settles with the freight partner, restocks inventory, keeps everything moving. When the customer pays 55 days later, the provider releases the remaining balance after taking a financing fee.

So for roughly $7,500 to $9,000, the business had access to $240,000 in working capital for just under two months. Operations didn't skip a beat.

That's the practical reality of invoice financing at work.

What Invoices Qualify for Invoice Financing?

Not every invoice will be accepted, and it's worth knowing what providers actually look at before you approach one.

Generally speaking, eligible invoices are:

Issued to other businesses (B2B), not to individual consumers

For goods already delivered or services already completed

Free from active disputes, credit holds, or partial offsets

Tied to buyers who can be identified and whose creditworthiness can be assessed

Conditional invoices, anything with an active dispute behind it, or invoices issued between related entities typically won't qualify. Some providers also set minimum invoice values, and a few want to see at least some invoicing history before opening a facility.

The cleaner your receivables book, the quicker and smoother the invoice financing process tends to be.

Who Is Invoice Financing Best Suited For?

The honest answer: any business that sends invoices and then waits. But let's be more specific, because the fit is especially strong in certain sectors.

Manufacturing Production doesn't stop because the previous batch hasn't been paid for yet. Invoice financing keeps the factory floor funded while payment clears.

Wholesale and distribution You restocked the shelves, the customer has 60 days to pay, and your supplier wants payment in 30. That mismatch is exactly what accounts receivable financing was designed for.

Import-export businesses Cross-border payment cycles are long. Add currency clearing times, customs delays, and international banking, and you're often looking at 90 days or more. Invoice financing within supply chain finance structures is standard practice here.

Freight and logistics You delivered the shipment. The invoice is out. But payment won't arrive for weeks. Invoice financing fills that window without disrupting operations.

Staffing and professional services Same problem, different industry. You've placed the staff, delivered the project, sent the invoice. Now you wait. You don't have to.

Benefits of Invoice Financing

There's a reason invoice financing has been around in various forms for well over a century. It solves a real and recurring problem.

Cash in days, not months. The most immediate benefit. Instead of a 60 or 90-day wait, most providers can advance funds within 24 to 48 hours of invoice approval. For a business managing tight cash cycles, that speed genuinely changes what's possible.

Your buyers' credit matters more than yours. Approval is based primarily on the creditworthiness of the businesses paying your invoices. That opens the door for growing businesses that wouldn't qualify for a traditional bank loan.

No equity given up. This is short-term working capital, not investment. Invoice financing doesn't dilute your ownership or bring anyone else to the table.

Grows with your business. As your invoicing volume increases, so does your access to the facility. You're not locked into a fixed borrowing limit that becomes a ceiling the moment business picks up.

Suppliers get paid on time. That one matters more than it might seem. Consistent, on-time payment often translates into better credit terms, volume discounts, and stronger relationships with the suppliers you depend on most.

You only use what you need. With selective invoice financing, you're not obligated to finance every invoice. Draw on the facility when it makes sense, leave it alone when it doesn't.

Invoice Financing vs Business Loans

| Factor | Invoice Financing | Business Loan |

|---|---|---|

| What it's based on | Unpaid invoices / receivables | Borrower's creditworthiness |

| Speed | 24 to 48 hours typically | Days to several weeks |

| Repayment | Tied to when your buyer pays | Fixed schedule regardless |

| Collateral needed | Invoices are the security | Often requires hard assets |

| Cost structure | Fee per invoice or on amount used | Interest on full loan balance |

| Flexibility | Draw only what you need | Fixed disbursement upfront |

| Debt impact | Off-balance-sheet in some structures | Adds to long-term debt obligations |

Purchase Order Financing vs Invoice Financing

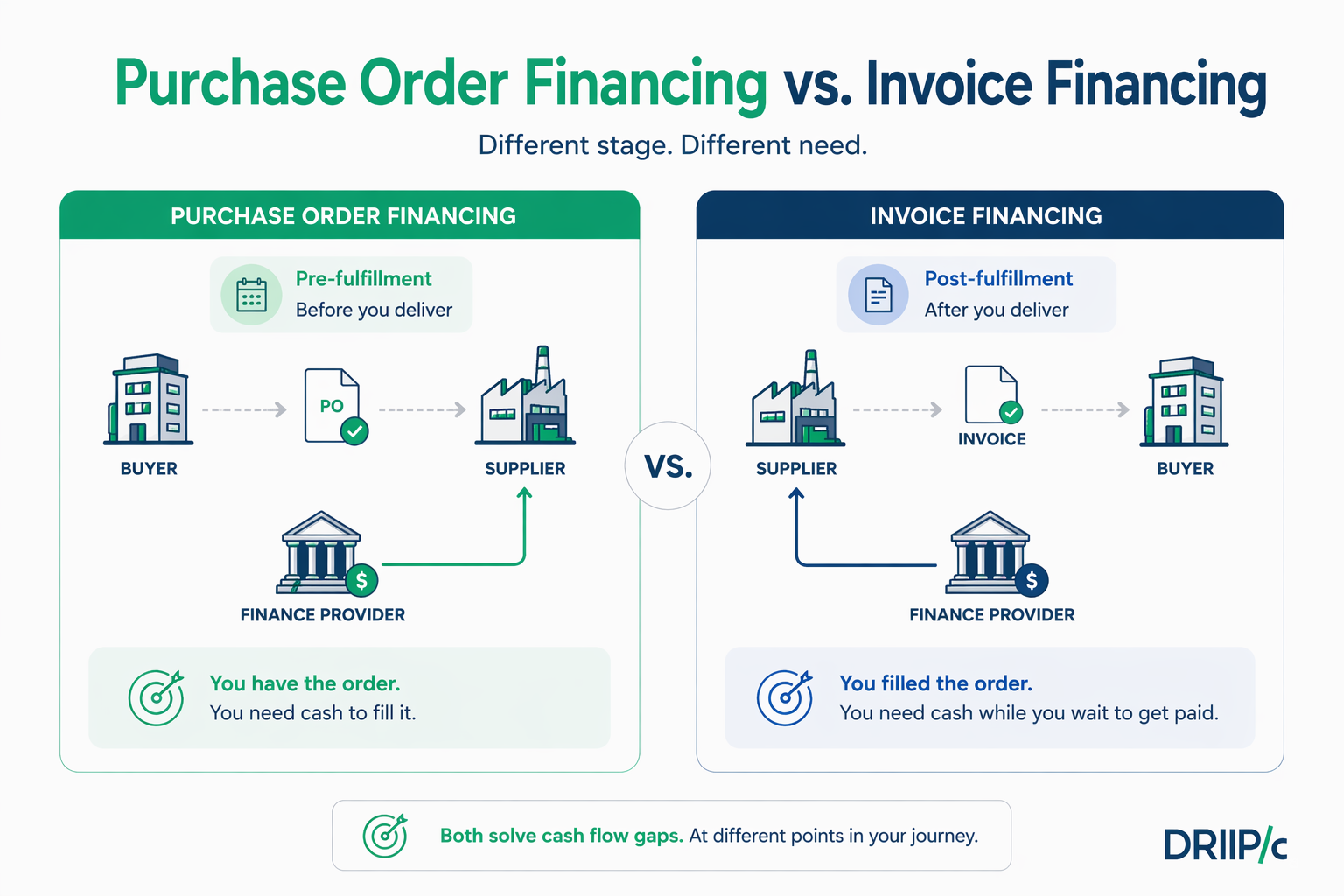

These two get conflated a lot, probably because both involve unfulfilled payments. But they sit at opposite ends of the business cycle.

Purchase order financing is pre-fulfillment. You've got a confirmed order from a buyer but you don't have the cash to pay your supplier and actually produce or procure the goods. A PO financing provider steps in and pays your supplier directly, so you can fulfill the order.

Invoice financing is post-fulfillment. The work is done. The invoice is out. With invoice financing, you don't have to just wait for the customer to pay.

Put plainly: PO financing = "I have the order. I need cash to fill it." Invoice financing = "I filled the order. I need cash while I wait to get paid."

Purchase Order Financing vs Invoice Financing Comparison

| Purchase Order Financing | Invoice Financing | |

|---|---|---|

| When it's used | Before fulfillment | After fulfillment |

| Backed by | A confirmed purchase order | An issued invoice |

| Who gets paid directly | Your supplier | Your business |

| Risk to the provider | Higher (goods not yet delivered) | Lower (delivery already confirmed) |

| Cost | Typically higher | Typically lower |

Invoice Financing vs Invoice Factoring

These two terms are often used as if they mean the same thing. They're related, but they're not identical.

Invoice factoring is actually a type of invoice financing, but with one significant structural difference: the factoring company buys your invoices outright and takes over the job of collecting payment from your customers. Your buyers will know about it. The factoring company will be in direct contact with them.

With invoice discounting, none of that happens. Your customers pay you as normal. You handle your end of the repayment with the provider. Nobody outside your business needs to know the arrangement exists.

Three things usually drive the choice:

Who you want to collect. If you want to stay in control of your customer relationships, discounting. If you're fine handing that off in exchange for less admin, factoring. Whether confidentiality matters. In some industries, a client finding out a third party is involved in their invoice processing is a non-issue. In others, it can raise questions you'd rather not answer.

How involved you want to be. Factoring is simpler in terms of day-to-day management. Discounting requires you to stay on top of collections yourself.

Both are forms of accounts receivable financing. Both use outstanding invoices to unlock working capital. The outcome is the same. The path there differs.

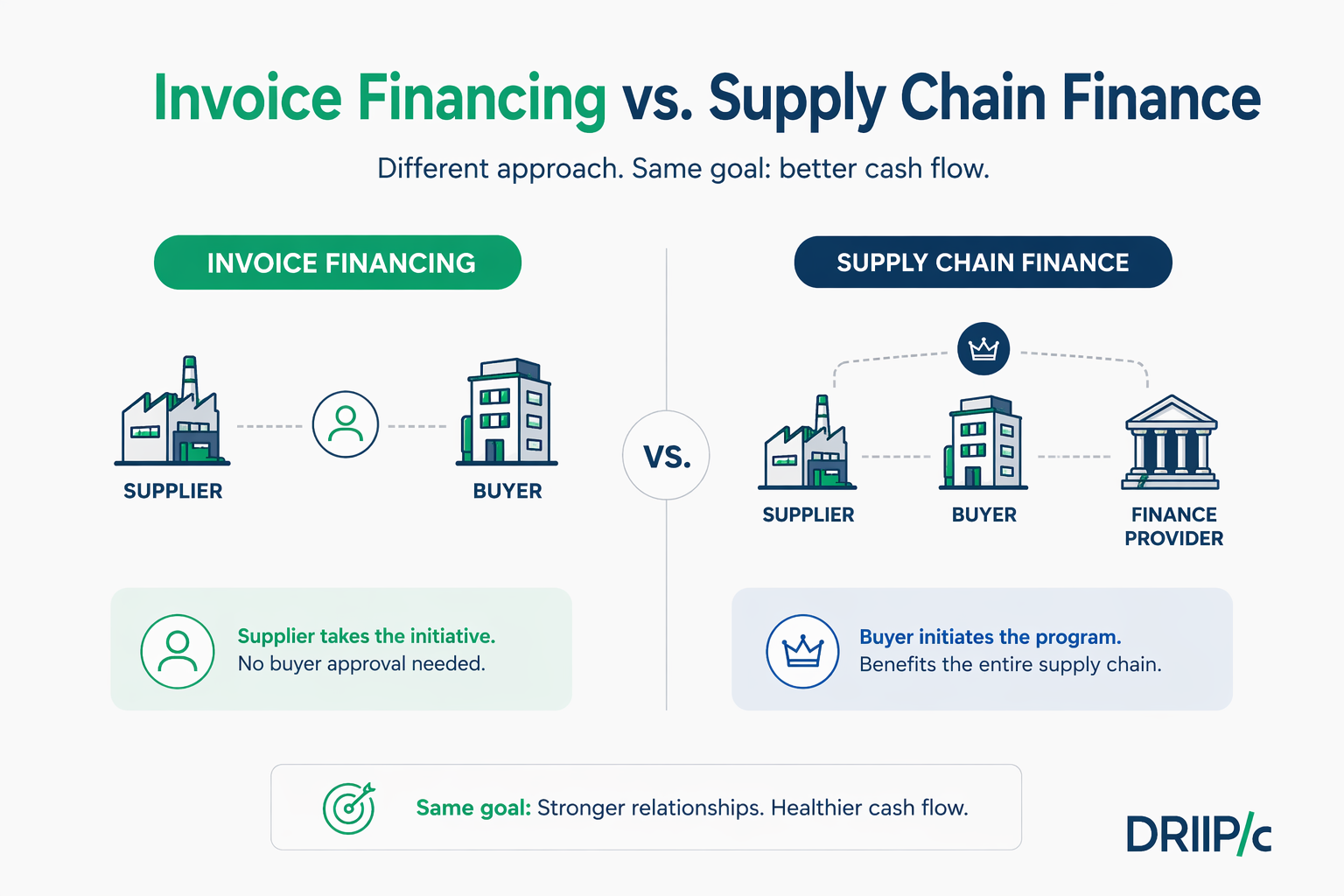

Invoice Financing and Supply Chain Finance: What's the Connection?

Supply chain finance, sometimes called supplier financing or reverse factoring, is a broader working capital category that optimizes cash flow across an entire supply chain, not just for one party in a transaction.

Invoice financing lives within that ecosystem but operates differently.

In a typical supply chain finance program, the buyer is the one who sets it up. They partner with a finance provider who agrees to pay their suppliers early at a slight discount. The buyer then repays the provider on their original extended terms. Both sides benefit, the supplier gets cash faster, the buyer keeps their long payment terms.

Invoice financing flips that. It's the seller, the supplier, who reaches out to the provider independently. No buyer buy-in needed. No program to join.

Invoice Financing vs Supply Chain Finance Comparison

| Invoice Financing | Supply Chain Finance | |

|---|---|---|

| Who starts it | Seller / supplier | Buyer |

| Buyer's role | Not required at all | Central to the whole structure |

| Who benefits most | Primarily the supplier | Designed to benefit both sides |

| Where it fits | Individual business cash flow | Enterprise-level procurement programs |

Cost of Invoice Financing: What You Actually Pay

Pricing varies across providers, but the general structure is consistent enough to explain clearly.

Discount rate or factor fee This is the main cost. Usually 1% to 5% of the invoice value per month, depending on the size of the invoice, how long until the buyer pays, and the buyer's credit profile.

Service or administration fee Some providers charge a flat fee per invoice or a monthly facility fee on top of the discount rate. Not all do, but it's worth asking.

Advance rate The percentage they advance upfront affects your effective cost. An 80% advance means 20% is held back until the buyer pays. Factor that into your planning.

Here's what it looks like in practice: You have a $100,000 invoice. The provider advances 80%, so $80,000 hits your account. The discount rate is 2.5% per month. Your buyer takes 60 days to pay. That's two months at 2.5%, so roughly $5,000 in fees. When the buyer pays, you receive the remaining $15,000 minus that $5,000, leaving you with $10,000.

Total cost: $5,000 to access $80,000 for two months. About 5% for a two-month facility.

Whether that's worth it depends on what you do with the $80,000. If it lets you fulfill a bigger order, avoid a late payment penalty, or keep a key supplier relationship intact, the math usually works out.

One thing worth doing: always ask providers for the APR equivalent, not just the monthly rate. It makes comparison across invoice financing providers significantly easier.

Invoice Financing for Small Businesses

There's a common assumption that invoice financing is a tool for larger businesses with established credit facilities and high invoice volumes. That's not accurate.

Invoice financing for small businesses is actually one of the most accessible forms of business funding available, and in many cases it's easier to qualify for than a conventional bank loan.

Here's why. Bank loans typically rely heavily on your own credit history, your assets, how long you've been in business. Invoice financing looks at your buyers instead. If you're a two-year-old business with a solid client roster that pays reliably, you have a real shot at qualifying even if your balance sheet isn't impressive yet.

The Fed's Small Business Credit Survey (2025) flagged cash flow timing as one of the top three financial challenges for small businesses in the US. That's exactly the problem invoice financing addresses.

And practically speaking, the onboarding process is far lighter than a bank loan. No months-long underwriting review. No property to put up as collateral. No audited financials going back five years. For small businesses that need to move quickly, that matters.

When Should a Business Consider Invoice Financing?

Invoice financing isn't the right answer for every situation. But there's a specific set of circumstances where it consistently makes sense.

It's worth exploring when:

Your customers are paying on 60 or 90-day terms and your suppliers want payment in 30

You've won a larger contract than usual and need capital to fulfill it before the last one settles

Cash flow dips every quarter due to seasonal demand, even though annual revenue is strong

One big buyer is running late on a large invoice and it's affecting everything else downstream

You want short-term liquidity without adding to your long-term debt load

The one thing worth saying clearly: invoice financing works best when it's planned, not panicked. Businesses that build it into their working capital strategy from the start, rather than scrambling for it in a crisis, tend to get better terms and use it more effectively.

What to Watch Out for Before You Sign

Like any financial product, the headline terms and the fine print don't always tell the same story. A few things worth checking before you commit to an invoice financing arrangement.

Concentration limits

Recourse vs non-recourse

Minimum monthly volumes

Dilution

Notification requirements

A provider who's upfront about all of this from the start is usually a better long-term partner than one who glosses over the details. If you're getting vague answers to direct questions, take that seriously.

Frequently Asked Questions About Invoice Financing

What's the difference between invoice financing and invoice factoring?

Factoring is receivables someone buys the invoices your customers owe you and chases payment themselves. Invoice financing is payable: a provider pays your supplier invoices and you repay them. Opposite sides of the transaction.

Does invoice financing affect my credit score?

Usually not the way a loan would. It's not reported as traditional debt in most structures. Still worth confirming with your specific provider.

How fast can I actually get funds?

24 to 48 hours once approved. First time might be slightly longer for verification. After that it's quick.

Is this the same as a working capital loan?

No. A loan gives you a lump sum and charges interest from day one. Invoice financing is transaction-based you use it for a specific invoice and repay within 90 days. You're not borrowing speculatively.

Can small businesses with poor credit use invoice financing?

Yes, often. Approval is based on your business and vendor relationships, not just your credit score. Easier to qualify than most bank products.

Is it useful for businesses that deal internationally?

Very much. Cross-border payments take time, customs adds delays, and working capital gets squeezed fast. Invoice financing fits well within international supply chain finance setups.

What does it actually cost?

Fees typically range from 1% to 4% of the invoice value depending on the amount and repayment window. Always ask for the full cost including any service fees, not just the headline rate.

Will my supplier know I'm using invoice financing?

No. From their end, they just get paid on time. The arrangement stays entirely in the background.

Conclusion: Invoice Financing as a Working Capital Strategy

A profitable business can still run out of cash. It happens because profitability and liquidity aren't the same thing. Revenue is one thing. Having that revenue available when you need it is another.

Invoice financing doesn't fix every cash flow problem. But for the specific and very common problem of waiting on invoices while expenses pile up, it's one of the most practical tools available. It's faster than a loan, doesn't require equity, grows with your business, and keeps supplier relationships intact.

The best businesses using invoice financing today aren't doing it reactively. They've built it into their working capital strategy as a standing facility they can draw on when timing demands it.

That's the right way to use it.

Drip Capital Invoice Financing

Drip Capital offers invoice financing designed specifically for businesses in trade, manufacturing, and wholesale that need working capital that actually moves at the speed of business. Over $9 billion in trade transactions facilitated. More than 11,000 businesses across the globe.

What the facility offers:

Funding limits up to $3 million

Disbursal within 24 to 48 hours of approval

Collateral-free access with no UCC blanket lien filing

Minimal documentation and a straightforward digital process

Transparent fees with no hidden charges

Want to understand what invoice financing could look like for your specific situation? Our team is happy to walk you through it.

For immediate assistance and tailored financial guidance, speak directly with a finance specialist.Call us on +1 (650) 437-0150.