Working capital is the excess of current assets over current liabilities. Working capital financing is the credit used to fund business investments in short-term assets such as accounts receivable and inventory.

It provides adequate liquidity and enables a business to fund its day-to-day operations like payroll, rents, overhead and other expenses.

Growing companies, companies with irregular business patterns & companies with a high seasonality opt have regular requirements for working capital loans to meet liquidity requirements between cycles.

This has given rise to a number of innovative financing products and some of these fall under the purview of inventory financing that leverages the inventory of any retailer, wholesaler, buyer or distributor against an advance of or a loan.

Inventory finance is a fairly broad term that has several sub-types & classifications.

What Is Inventory Financing?

Inventory financing is asset backed financing where a business obtains a loan or an overdraft against the company’s own inventory as a collateral.

The financing can be obtained against whole or partial inventory. The financier provides funds for a certain percentage of inventory - usually 50%-90% of the inventory value.

The terms and conditions of the financing differ from financier to financier and depend predominantly on the volume of inventory, inventory turnover ratio - the number of times a business sells or replaces their inventory in a given period, sales level etc.

The repayment period is usually anywhere from 2-12 months but can extend up to 36 months in some cases.

The expected annual interest rate wildly depends upon factors like the borrower’s financial history, credit score, going time of the enterprise etc in addition to inventory value and turnover ratios.

There are additional charges like inventory appraisal fees, origination fees, prepayment penalties levied by the financier on inventory financing etc.

Types of Inventory Financing

Here are the 4 main types of inventory financing options available to a borrower.

Warehouse Financing

This form of inventory financing is almost always extended towards manufacturers or parties closer to the supply chain.

In this form of financing, the borrower will have to move the entire inventory (against which the advance is being extended) to a warehouse facility.

The financial institution usually extends some control over the movement of goods from the warehouse facility. This type of inventory financing is quite common in commodity businesses.

Loan for Inventory

Inventory financing is popularly associated with borrowing money against the inventory resale value of the available inventory. However, several, upstart and smaller businesses also require financial capital for purchasing inventory for resale in the first place. This is where Loans for Inventory purchases come in.

Lenders typically use the inventory itself as collateral but also insist on a certain amount of down-payment against the inventory value. The interest rates for such loans typically are around the same rates as the prevailing benchmark rates.

Loan against Inventory

This is a simple, traditional type of loan where the financier grants a short-term loan as a certain percentage of the value of the business inventory.

If the business defaults on the loan, the financier takes charge of the inventory and recovers the money due by selling this inventory.

It is often used as a international buyer finance solution wherein an importer can gain access to cash required to cover domestic selling expenses, operational expenses etc by staking the inventory as collateral.

Some financing solutions also pay the suppliers directly instead of sending funds to the borrower. The financiers collect repayment in monthly installments, or as a percentage of sales.

Inventory Line of Credit

Under this arrangement, the lender sanctions a credit limit to the business based on the inventory value. The business can withdraw cash, as many times depending upon the requirement till the total sanctioned limit, but not above it.

The business owner can repeat this cycle over and over, as long as they make the minimum required repayments – the system operates just like credit cards. The interest rate is charged only on the actual amount withdrawn from the total sanctioned limit. In most cases, there is a small processing fee attached to the total facility as well.

If the business defaults on the loan, the financier can seize the inventory and make up for the lost payment. When the line of credit expires, the full amount due is broken down for repayment as with a bank loan.

Most of these inventory financing solutions, with the exception of Loans for inventory, are quick financing products where it is possible to access the funds within 48 hours. However, a more realistic time-line would be somewhere between 4-5 days.

Inventory Factoring

This is a financing arrangement where a business with a healthy order flow and sales cycle approaches a lender to discount its purchase orders precisely to be able to purchase inventory for catering to these orders.

A relatively novel trade finance technique, this method has numerous benefits. For one, the lender can draw comfort from the volume of purchase orders as it is indicative of market demand for the client's goods and services.

The borrower also benefits as most inventory factoring solutions do not seek collateral from the borrower.

Drip Capital's Inventory Financing services are mostly based on this reverse factoring process that allow borrowers to secure fast financing to fulfill their orders relatively quickly.

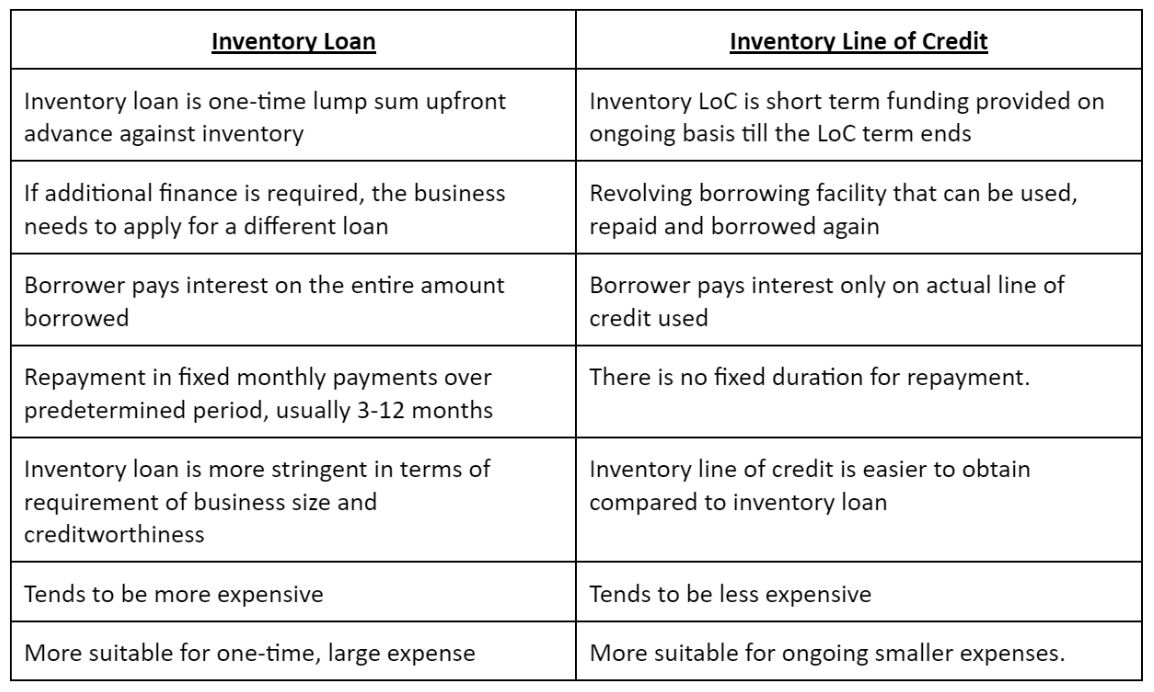

Key Difference Points between Inventory loan and Inventory Line of Credit

Alternatives to Inventory Financing For an Importer

In addition to Inventory financing there are other modes of working capital finance like Receivable Financing, Payable Financing and Working Capital loans which can possibly turn out to be a more cheaper & convenient solution.

Bill Discounting A fairly well known form of financing, bill discounting is essentially a loan that is advanced to the borrower against the borrower’s trade receivables.

Unsecured Working Capital Financing Some financers also offer unsecured lines of credit also referred to as a business line of credit. These unsecured lines are usually targeted toward small businesses.

Accounts Payables Financing:

An accounts payable financing arrangement, in its simplest form, is a technique where buyers seek financing for procuring goods in order to cater to an incoming order. There are mainly two types of payables finance solutions that a borrower can secure.

- Vendor Finance: Under this arrangement, the supplying company itself ships the goods to the buyer in advance without upfront payments. It is also known as vendor notes or vendor loans.

For this service the vendor charges either a premium on the sale price of the goods or a fixed interest rate from the borrower. We've covered this guide on vendor financing if you with to know more.

- Supply Chain Finance: This is an ideal solution for relatively large sized importing companies with numerous suppliers across the globe. Instead of periodically arranging for payments for every supplier each time an order is made, a supply chain finance company ensures that the vendors have the flexibility to discount the invoices against the supplier while also relying on the credit profile of the importing company (which is generally healthier). There are two main advantages to this.

For one, the suppliers can choose to factor their invoices as per their cash flow position. The buyer will charge a fee for suppliers who discount their invoices earlier and waive the fee for suppliers who don't discount them. This is called dynamic discouting. The flexibility and convenience of the entire supply chain financing process ensures all parties are satisfied.

Secondly, since the advances are provided against the credit profile of the buyer, the interest rates the suppliers end up paying is far lesser than if they were to secure the loan by themselves.

FAQs

1. What are the costs involved in inventory financing? A: Inventory financing includes Loan application fees (Upfront fees to be paid while applying for the loan), Appraisal fees (Cost of appraisal of inventory that the financier will undertake), Early repayment fees, Late payment fees

2. How much interest is charged for inventory financing by financiers? Significantly depends on the risk-profile of the borrower, tenure, years in business but can typically range from 12% to as much as 40% per year.

3. When does inventory financing make sense? Inventory financing makes sense when a business has a high inventory turnover ratio i.e. a high turnaround time before converting inventory into sales. This can include machinery, furniture, art etc where the importer generally takes a fair amount of time to find new buyers.