A line of credit is often spoken about as a single product, but in reality, it is a category of financing options built in different ways for different needs. The structure you choose can affect how quickly you access funds, how much control you have over usage, and how well the financing fits your day to day operations.

For many businesses, especially those operating in the $2 million to $8 million revenue range, the difference between one type of credit line and another is not just technical. It can determine whether orders are fulfilled on time, whether suppliers are paid without delay, and whether growth opportunities are captured or missed.

This is why understanding the different types is not just useful. It is necessary.

What Actually Changes Across Different Types of Line of Credit?

At a surface level, all lines of credit look similar. You get approved for a limit, you draw funds, and you repay. But once you go deeper, the differences become clear. Some credit lines are tied to assets. Others depend purely on business performance. Some give full freedom in how funds are used, while others are linked to specific transactions like invoices or inventory.

These differences influence three important things:

- how much capital you can access at a given time

- how quickly you can access it

- how much control you have over using it

A business that needs $100,000 today and another $80,000 next month will value flexibility very differently from a business that borrows against fixed receivables.

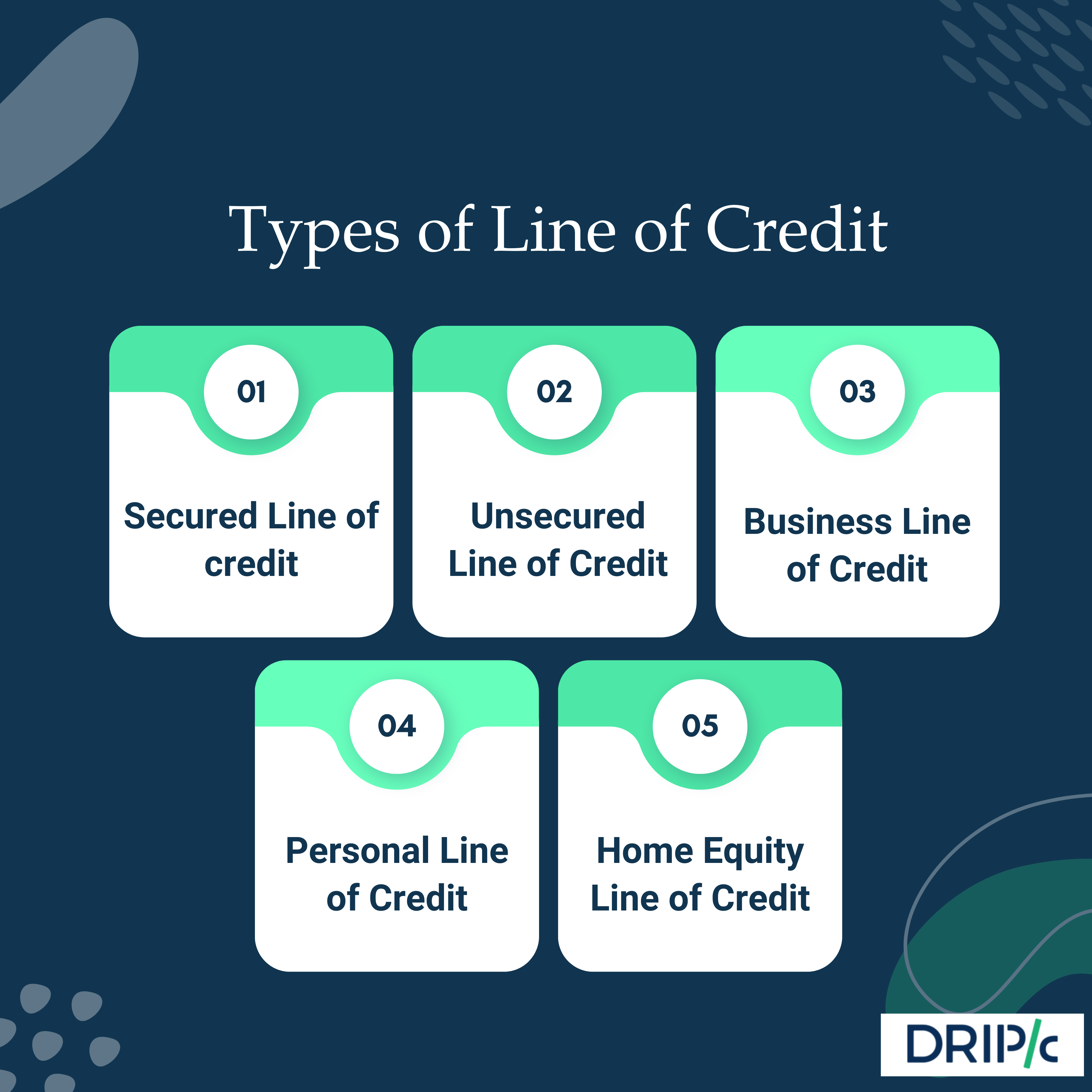

Secured Line of Credit

A secured line of credit is built around assets. Lenders offer capital against inventory, receivables, or equipment, which reduces their risk and often results in lower interest rates.

In most cases, businesses using this structure see interest costs in the range of 7 percent to 14 percent annually, depending on asset quality and financial strength. For companies with strong receivables and stable operations, this can be a cost effective option.

But the trade off is flexibility. The credit limit is not fully independent. It is linked to the value of the assets backing it.

If receivables drop from $500,000 to $320,000 over a quarter, the available credit may reduce accordingly. This can create limitations during periods of growth or fluctuation.

This type of credit line works best when:

- asset levels are stable and predictable

- borrowing needs closely follow operational cycles

- cost savings are more important than flexibility

Unsecured Line of Credit

An unsecured line of credit removes the need for collateral entirely. Approval is based on financial performance rather than assets, which changes how the product behaves in real use. Businesses with stable revenue and consistent cash flow are typically strong candidates for this type of credit. Credit limits can range from smaller working capital amounts to higher limits depending on financial strength and repayment capacity.

The key advantage is control. Funds are not tied to specific invoices or inventory. They can be used across different needs without additional approvals.

A business might use:

- $70,000 for inventory this month

- $40,000 for payroll in the next cycle

- $30,000 for marketing during peak demand

All within the same facility, without restrictions. Interest rates are usually slightly higher than secured options, often ranging between 10 percent to 20 percent annually. However, many businesses accept this difference because it allows them to operate without constraints.

Business Line of Credit

A business line of credit is structured specifically for working capital. It is one of the most widely used forms of financing for companies that deal with ongoing expenses and uneven cash flow timing.

In industries such as wholesale, ecommerce, and manufacturing, it is common for payments to come in after 30 to 60 days while expenses must be paid earlier. This creates a gap that needs to be managed consistently.

A business line of credit fits directly into this pattern.

It is commonly used for:

- inventory purchases ahead of demand cycles

- supplier and vendor payments

- payroll during slower receivable periods

- short term operational expenses

For example, a company generating $4 million in annual revenue may use a $300,000 credit line to maintain inventory flow. Over a 60 day period, this can improve order fulfillment rates by 15 to 20 percent simply because stock availability is maintained.

Personal Line of Credit

A personal line of credit is designed for individual use and is evaluated based on personal income and credit history.

It offers flexibility for expenses such as home improvements, emergency costs, or short term financial gaps. Limits are usually smaller compared to business credit lines, often ranging between $10,000 to $100,000 depending on creditworthiness.

While it may seem convenient, using personal credit for business purposes can create complications. It mixes financial records and makes it harder to track performance or claim business expenses accurately.

For structured operations, keeping business and personal financing separate is always a better approach.

Home Equity Line of Credit

A home equity line of credit uses residential property as collateral. The available credit depends on the value of the property and the equity built over time.

This type of credit line often comes with lower interest rates, sometimes between 6 percent to 10 percent annually, because it is backed by a physical asset.

However, the risk is significantly higher. The asset securing the credit is personal property. Any repayment issues can directly impact ownership.

It is generally used for:

- large personal expenses

- home renovation projects

- long term financial needs

While some business owners consider using it for working capital, it is rarely the safest choice due to the personal risk involved.

Comparing Different Types of Line of Credit

| Type | Collateral | Flexibility | Typical Cost Range | Best Fit |

|---|---|---|---|---|

| Secured | Yes | Moderate | 7 percent to 14 percent | Asset based businesses |

| Unsecured | No | High | 10 percent to 20 percent | Growing businesses |

| Business Line | Sometimes | High | Varies | Working capital |

| Personal | No | Moderate | Depends on credit score | Individual use |

| Home Equity | Yes | Limited | 6 percent to 10 percent | Property backed borrowing |

| Invoice Based | Yes | Limited | Variable | Receivable driven businesses |

Line of Credit vs Credit Card

A credit card is often considered a form of line of credit because it allows access to funds up to a pre approved limit, with the option to repay over time. However, in real financial use, the two serve very different purposes.

A line of credit is typically structured for planned or recurring financial needs, while a credit card is designed for everyday transactions and short term spending. The difference becomes more noticeable as the size and frequency of funding requirements increase.

| Feature | Line of Credit | Credit Card |

|---|---|---|

| Interest rates | Typically lower, depending on structure and risk | Higher, often ranging from 24 percent to 36 percent annually |

| Usage purpose | Designed for working capital and larger expenses | Used for daily spending and smaller transactions |

| Credit limit | Generally higher, based on financial strength | Usually lower compared to credit lines |

| Repayment structure | Structured repayments, often monthly | Minimum payments with flexible repayment |

| Cost efficiency | More efficient for larger amounts over time | Can become expensive if balances are carried |

| Flexibility in usage | Can be used for a wide range of financial needs | Best suited for short term usage |

| Impact on operations | Supports business cash flow and planning | Limited use for operational funding |

In practical terms, credit cards are useful for convenience and short term liquidity. A line of credit, on the other hand, is better suited for managing ongoing financial needs where larger amounts and structured repayment matter. For businesses, the distinction is important. Relying on credit cards for operational funding can quickly become expensive, while a line of credit provides a more stable and predictable way to manage cash flow.

How to Choose the Right Type for Your Situation?

Choosing the right line of credit is about how your business actually runs, not just what looks good on paper. The structure should match your cash flow, not fight it.

Think in practical terms:

- If your cash flow is steady and backed by receivables or inventory, a secured line of credit can work well and usually comes at a lower cost

- If your expenses change month to month and you need freedom to use funds across operations, an unsecured line of credit is a better fit

- If your focus is day to day working capital like payroll, suppliers, and inventory cycles, a business line of credit makes the most sense

- If your needs are personal or smaller in scale, a personal line of credit is more appropriate

- If you are considering using property to access larger funds at a lower rate, a home equity line of credit may be an option, but it comes with personal risk

- If your business depends heavily on invoices and long payment cycles, invoice based financing can help with timing, but it limits flexibility

A simple way to approach the decision:

- Predictable operations → structured and asset backed options

- Variable expenses → flexible and unsecured options

- Lower cost priority → secured structures

- Speed and ease of access → unsecured or fintech options

In most cases, the right choice becomes clear when you map the credit structure to how your business actually uses money on a monthly basis.

Why Structure Matters More Than You Think?

Two businesses may have access to the same credit limit but experience very different outcomes depending on structure.

One may face delays because its credit is tied to assets. Another may move faster because it has full access without restrictions.

In fast moving industries, this difference becomes visible quickly. Businesses that can access capital without delays are often able to respond better to demand and maintain consistency in operations.

Frequently Asked Questions

Which type of line of credit is most flexible

Unsecured credit lines generally offer the highest flexibility because they are not tied to assets or specific transactions.

Which option is more cost effective

Secured credit lines usually have lower cost due to reduced risk for lenders.

Can a business use more than one type

Yes, many businesses use a mix depending on their needs and growth stage.

What type is best for working capital

A business or unsecured line of credit is typically the most practical option.

Conclusion

A line of credit is not a single solution. It is a set of options designed to meet different financial needs. The type you choose affects how you operate, how you manage cash flow, and how quickly you can respond to opportunities.

For businesses that are growing and dealing with ongoing capital requirements, flexibility often becomes more valuable than cost alone. The right structure allows you to access funds when needed, use them without restrictions, and maintain control over operations.

Understanding these differences helps in choosing a solution that supports both stability and growth.

Drip Capital’s Line of Credit

For businesses that need reliable access to working capital without operational restrictions, Drip Capital’s line of credit is designed to provide flexibility and control.

It offers a fully drawable limit, allows funds to be used across inventory, payroll, and supplier payments, and does not place any lien on business assets. Each draw follows a structured monthly repayment, and credit becomes available again as repayments are made.

With line sizes up to $1 million and funding available within 24 hours after a draw request, it supports businesses that require consistent access to capital.

Also Read

Advantages & Disadvantages of Line of credit

For immediate assistance and tailored financial guidance, speak directly with a finance specialist.Call us on +1 (650) 437-0150.